Startup Development Stages: From Early-Stage to IPO

Early-Stage to IPO | Understanding the Different Phases of Startup Development and Growth

.jpg)

Introduction: Understanding the Stages of Startup Development – A Structured Reading of Growth

The evolution of a startup is rarely linear. It unfolds along a trajectory shaped by experimentation, validation, expansion, and, for some, access to financial markets. Yet the terms commonly used to describe these stages — Early-stage, Seed, Series A, Series B, Scale-up, IPO — are often applied without a clear distinction between economic maturity and funding sequence. A startup can be defined as an organization searching for a scalable and repeatable business model in a highly uncertain environment (Blank & Dorf, 2012).

What Are the Stages of Startup Development?

The stages of startup development correspond to the different phases of its life cycle, from the initial idea (early-stage) to an eventual initial public offering (IPO). Each stage — Seed, Series A, Series B, Scale-up — reflects a specific level of economic and organizational maturity.

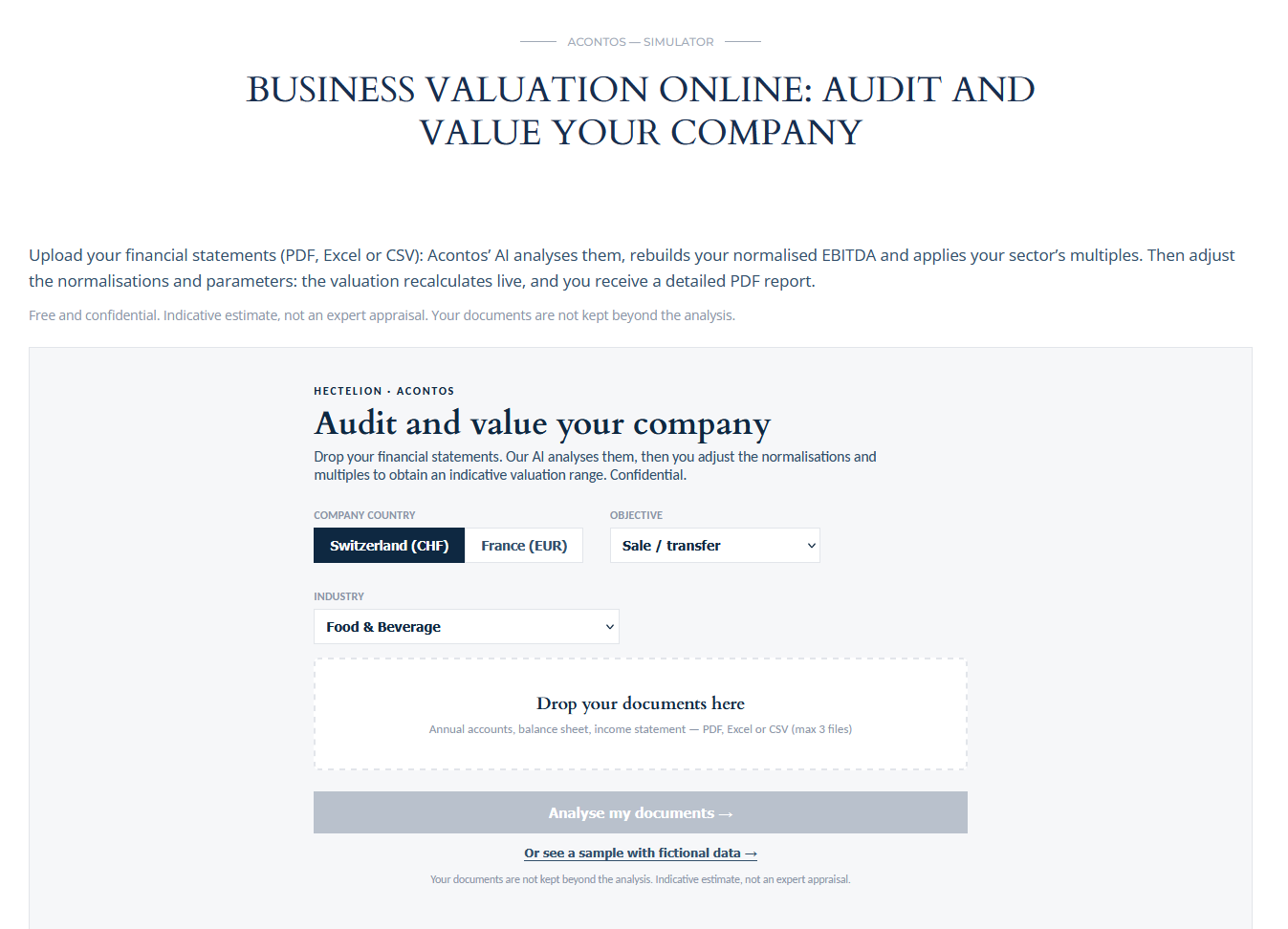

Would you like to have your business valued or raise funds?

Hectelion conducts independent valuations and supports fundraising in France and Switzerland.

→ Book a call — 30 minutes, confidential

From Early-stage to IPO: A Structured Reading of Development Phases

The evolution of a startup can be understood as a succession of stages marked by progressive transformation of its business model, organization, and capital structure. In its initial phase, a startup explores a problem and attempts to identify a viable solution (Early-stage). The following phase (Seed) marks the transition from exploration to validation. Series A occurs once product-market fit has been established. Series B corresponds to a broader expansion phase. The notion of scale-up describes the stage at which growth becomes repeatable and structured. Series C and subsequent rounds typically fall within a consolidation and strategic preparation logic. The IPO represents the culmination of this cycle.

Early-stage (Pre-seed): Exploration Under Maximum Uncertainty

The Early-stage marks the starting point of the startup development cycle. The company operates in an exploratory logic: identifying a relevant problem, formulating a credible value proposition, and testing technical feasibility. The business model is not yet stabilized, and future cash flows remain largely hypothetical. Early-stage is therefore foundational: the priority is learning, not optimization.

Seed: Model Validation and Initial Market Traction

The Seed phase marks the transition from exploration to validation. Early revenues, active users, initial partnerships, or engagement metrics provide tangible signals confirming the relevance of the value proposition. The objective is not yet to optimize profitability, but to prove that the model can function at a small scale.

Series A: Structuring and Accelerating a Validated Model

Series A occurs once the startup has reached a decisive milestone: the business model has been validated by the market. The organization must professionalize, teams expand, responsibilities become clearer, and processes are formalized. Series A finances the scaling of a validated model.

Series B: Expansion and Growth Industrialization

Series B corresponds to an expansion phase where growth is no longer merely demonstrated but becomes repeatable. The company must now change scale, standardize processes, and move from a founder-centric entrepreneurial structure toward a more hierarchical and specialized organization.

Scale-up: Sustained and Structured Growth

The concept of a scale-up does not refer to a specific funding round, but to an economic stage characterized by sustained and structured growth. According to the OECD definition of high-growth enterprises, this threshold corresponds to more than 20% annual growth over three consecutive years, with at least ten employees at the starting point. The scale-up phase represents a pivotal moment, distinguishing startups that move beyond expansion toward structured long-term development.

Series C: Strategic Consolidation and Exit Preparation

Series C takes place once the company has already passed through the stages of validation, structuring, and expansion. The objective is to consolidate an established position and prepare for a major strategic milestone. Series C represents the consolidation and pre-exit phase, marking entry into advanced maturity.

IPO: Institutional Transformation and Access to Public Markets

An Initial Public Offering represents a structural transformation rather than merely a financial event. The IPO marks the transition from privately funded ownership to a publicly listed company subject to the requirements of capital markets. This shift entails profound changes in governance, transparency, and operational discipline.

Valuation Methods According to Startup Development Stage

Appropriate valuation methodologies depend directly on the maturity of the business model, the quality of available data, and the dominant risk profile. In Early-stage, valuation relies on qualitative or semi-qualitative methodologies (Berkus Method, Scorecard Method, Risk Factor Summation). At Seed stage, the Venture Capital Method is widely used. From Series A, methodologies become more quantitative with revenue multiples and cautious DCF models. At scale-up or Series C, sector multiples and full DCF models become more defensible. In pre-IPO or IPO phases, valuation enters the realm of public markets.

Valuation methodology must therefore evolve alongside company maturity.

The Startup Development Cycle Path

CEO Statement

Understanding the stages of startup development requires intellectual coherence. Each stage corresponds to a specific level of economic maturity, a distinct risk profile, and a defined quality of available information. Rigor does not consist in using the most complex methodology, but in applying the most relevant one given the company’s development stage. Strategic discipline therefore rests on a simple principle: align analysis with the company’s real maturity.

Conclusion: Structuring Growth Through an Understanding of Development Phases

Startup development cannot be reduced to a succession of funding rounds. Understanding these stages makes it possible to anticipate the strategic, organizational, and financial challenges specific to each of them. Not all startups become scale-ups. The development cycle includes pivots, consolidations, strategic exits, and alternative paths.

Would you like to train in business valuation?

Hectelion offers business valuation training programmes.

👉 Learn more about the training

Author

Aristide Ruot, Ph.D. — Founder | Managing Director