WACC: Understanding, Calculating, and Using Cost of Capital

Core of financial valuation and investment decision

Introduction: Why WACC Is a Cornerstone of Corporate Finance

The weighted average cost of capital (WACC) occupies a central place in corporate finance. It is ubiquitous in valuation work, investment decision-making, mergers and acquisitions, and discussions with investors. Yet behind an apparently simple formula, WACC remains one of the most misunderstood and most mechanically applied concepts in financial practice.

By definition, WACC represents the rate of return required by all providers of capital—shareholders and lenders—to finance a company’s assets, given the risk associated with its business and capital structure. It is therefore the fundamental link between risk, financing, and value. When used as a discount rate, it directly drives valuation outcomes and, ultimately, the strategic decisions derived from them.

In practice, however, WACC is too often reduced to a purely technical, sometimes automated exercise. Parameters are selected without robust analysis, risk assumptions remain implicit, and adjustments are occasionally applied without a clear economic rationale. This approach can generate misleading results and poorly calibrated decisions, particularly in complex or non-standard contexts.

This raises a central question: how can WACC be built and used in a rigorous, coherent, and economically grounded way—beyond its mere mathematical expression?

This article provides an in-depth reading of WACC, revisiting its theoretical foundations, its key components, and their economic logic. It sequentially reviews the contexts in which WACC is used, the construction of the cost of equity and cost of debt, the role of taxation and capital structure, and then proposes an operational assembly of the full WACC. The analysis is complemented by a discussion of WACC’s limitations and the precautions required for interpretation, with the objective of making WACC a genuine decision-support tool rather than a mere calculation input.

Origins and Theoretical Foundations of the Weighted Average Cost of Capital

The concept of the cost of capital lies at the very foundations of modern finance. It originates in the pioneering work of Franco Modigliani and Merton Miller, who, in the late 1950s, laid the analytical groundwork connecting capital structure, risk, and firm value.

In their seminal 1958 paper, they show that in a perfect world—without taxes, transaction costs, or information asymmetries—a firm’s value is independent of its financing structure.

This neutrality disappears once realistic frictions such as taxation, default risk, or bankruptcy costs are introduced. At that point, each source of financing carries its own cost, and the combination of these costs becomes value-relevant. WACC then emerges as an economic synthesis of heterogeneous return requirements.

Economic Purpose and Operational Role of WACC

In professional practice, WACC is primarily used as the discount rate for free cash flows available to all capital providers. It translates the combined return requirements of shareholders and lenders—given the company’s business risk—into a single rate.

WACC therefore serves as a benchmark to assess whether a company creates or destroys value. A project whose economic return exceeds WACC contributes to value creation, whereas a return below WACC implies value destruction for capital providers. This logic is at the core of modern performance management frameworks, including metrics such as Economic Value Added (EVA).

This perspective is extensively documented in academic and professional literature, notably by Brealey, Myers, and Allen, for whom the cost of capital is the fundamental bridge between investment decisions and investors’ expectations.

Use Cases and Conceptual Boundaries of WACC

WACC becomes a core tool whenever future economic performance must be translated into present value, under the assumption that the company can be viewed as an asset generating relatively predictable cash flows. Its use implicitly assumes that the firm’s overall risk can be summarized by a single rate that represents the required returns of all capital providers.

In corporate valuation, WACC is the reference discount rate for free cash flows to the firm, typically within a discounted cash flow (DCF) framework. It converts the company’s ability to generate future economic cash flows into present value, independently of its instantaneous financing mix. This approach is especially relevant for mature companies or businesses in stabilized growth phases, with meaningful operating history and a relatively readable economic model. WACC’s robustness in this context stems from the consistency between the projected flows—generally operating cash flows before debt service—and a discount rate meant to remunerate both shareholders and lenders.

In M&A transactions, WACC plays a structuring role at several levels. It affects not only the intrinsic valuation of the target, but also synergy assessment, post-transaction financing arbitrage, and the comparison between standalone value and value to the acquirer. In an M&A context, WACC helps preserve analytical neutrality by separating the target’s economic value from the acquirer’s financing decisions. This neutrality is conditional on the assumption that the target’s business risk remains broadly unchanged after the transaction—an assumption that may not hold when deep operational transformations are contemplated.

WACC is also used in fundraising discussions, particularly when negotiating pre-money or post-money valuations for companies with established operations. In this setting, WACC helps formalize investors’ return expectations by linking them to observable market parameters such as the risk-free rate, the market risk premium, and sector risk profile. Its use becomes more delicate at earlier stages, where cash flows are highly uncertain, a target capital structure is not yet meaningful, and risk evolves materially over time. As Aswath Damodaran highlights, the cost of capital is only relevant if risk is relatively stable over the analysis horizon—a condition rarely met in early development stages.

Beyond transactions, WACC is widely used as a strategic decision-support tool, especially to arbitrate between investment projects or to measure economic value creation. Comparing a project’s expected return to WACC is effectively testing whether the project covers the opportunity cost of the capital employed. While conceptually sound, this requires the project’s risk to be comparable to that of the existing business. Otherwise, applying a single corporate WACC can bias decisions by undervaluing high-risk projects and overvaluing more defensive ones—a bias well documented in academic literature.

General WACC Formula and Underlying Economic Logic

WACC is built on a simple economic idea, but one that is demanding in practice: a company is financed by multiple categories of capital, each bearing a different level of risk and therefore a specific required return. WACC aggregates these heterogeneous requirements into a single rate that represents the firm’s overall cost of financing across all sources.

Formally, WACC is expressed as a weighted average of the cost of equity and the cost of debt, with weights reflecting the real economic contribution of each financing source to the overall capital structure. This is neither an arithmetic nor an accounting average; it is fundamentally economic because it relies on market values rather than historical or book values.

The general WACC formula is:

In this expression, E is the market value of equity, D is the market value of interest-bearing debt, Ke is the cost of equity, Kd is the pre-tax cost of debt, and T is the company’s marginal tax rate. Each term reflects a specific economic rationale, and together they form a coherent equilibrium between risk, return, and financing structure.

The first structuring element of WACC is market-value weighting. This is fundamental because financial markets express investors’ return expectations at any given point in time. Using book values would ignore the real economic conditions under which capital is employed. As Brealey, Myers, and Allen emphasize, the cost of capital must always be assessed from the investors’ perspective rather than from internal company accounting metrics.

The second pillar is the distinction between the cost of equity and the cost of debt. Equity holders bear the residual risk of the firm: they are paid after lenders and fully absorb variability in performance. In return for this higher risk, they require a higher return, which typically makes the cost of equity higher than the cost of debt. Lenders, by contrast, benefit from seniority and contractual compensation, resulting in a lower cost, albeit with exposure to default risk.

A third key element is the tax adjustment applied to the cost of debt. In most tax systems, interest expenses are deductible from taxable income, reducing the firm’s true economic cost of borrowing. The factor (1−T) is therefore not a mathematical convenience but the direct expression of a structural tax benefit that influences financing trade-offs and capital structure. This integration of taxation into WACC follows from Modigliani and Miller’s extensions once corporate taxes are introduced.

Conceptually, WACC can be interpreted as the minimum return required by all providers of capital to maintain the firm’s value. It is the opportunity cost of invested capital: if the firm earns exactly its WACC, it meets investors’ return requirements without creating or destroying value. Performance above WACC implies economic value creation; performance below WACC implies value destruction.

This economic interpretation explains why WACC is used as the discount rate for free cash flows to the firm. Because those flows are stated before remunerating debt and equity, the discount rate must reflect the cost of both sources simultaneously. Consistency between the numerator (operating flows) and the denominator (WACC) is a core condition for methodological validity.

Koller, Goedhart, and Wessels stress this point: WACC is not just a formula; it is a reasoning framework linking capital structure, business risk, and value. In this perspective, WACC acts as a synthesis mechanism compressing complex market, tax, and risk information into a single rate.

Cost of Equity (Ke): Construction, Inputs, and Economic Foundations

The cost of equity is the return required by shareholders to invest in a company given the risk they bear. Unlike lenders, shareholders do not benefit from contractual remuneration or repayment priority; they bear residual risk and are exposed to the full variability of operating and financial performance. In return, they require a return above that of risk-free assets. The cost of equity is typically the highest and most sensitive component of the overall cost of capital.

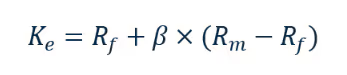

In professional practice, cost of equity is most commonly estimated using the Capital Asset Pricing Model (CAPM), known in French as the MEDAF. CAPM links required return to the company’s systematic risk—risk that cannot be diversified away and that is driven by broad market fluctuations.

CAPM is expressed as:

This relationship reflects a structured economic logic. The starting point is the risk-free rate Rf, which represents the minimum return required to defer consumption without default risk or uncertainty over future cash flows. Conceptually, it compensates only for the time value of money. In practice, it is proxied by long-term sovereign yields in the same currency as the cash flows. As Aswath Damodaran emphasizes, the choice of the risk-free rate is fundamental because it anchors the entire cost of equity construction.

To this risk-free return is added compensation for exposure to market risk, captured by the market risk premium (Rm−Rf)). The market return Rm corresponds to the return required to hold a broadly diversified equity portfolio representative of the investable market. The market risk premium therefore measures the additional compensation investors demand for bearing equity risk rather than holding risk-free assets. It reflects collective risk aversion and is among the most structuring inputs in the cost of equity.

CAPM further assumes that not all assets have the same exposure to market risk. This relative exposure is measured by beta β, which captures the sensitivity of the company’s returns to market returns.

- a beta of 1 implies market-like systematic risk.

- a beta above 1 implies amplified sensitivity to market movements.

- a beta below 1 implies a more defensive profile. Beta therefore amplifies or dampens the market risk premium in the cost of equity calculation.

It is important to note that the beta used in CAPM is a levered beta: it reflects both business risk and the effect of financial leverage. Shareholder risk depends not only on the economic risk of the business but also on leverage, which mechanically amplifies the variability of equity returns. The distinction between unlevered beta (asset beta, capturing pure business risk) and levered beta (equity beta, including financing effects) is central in corporate valuation practice and is formalized in Hamada’s work.

Risk-Free Rate (Rf): The Anchor of Required Return and the Starting Point of the Cost of Capital

The risk-free rate is the cornerstone of any cost of capital construction. It represents the minimum return required to defer consumption without default risk or uncertainty about future cash flows. Conceptually, it compensates only for the time value of money; it does not remunerate business risk, financial risk, or market uncertainty, which are addressed through risk premia.

Within CAPM and WACC, the risk-free rate plays a fundamental role because it is the common base upon which all risk compensation is added. Any inconsistency or approximation in the risk-free rate propagates mechanically throughout the cost of capital and ultimately impacts valuation. Selecting the risk-free rate is therefore not a matter of arbitrary convention but of disciplined economic reasoning.

In theory, a risk-free asset has a known future return with certainty and no default risk. In practice, such an asset does not exist, so markets rely on operational proxies—most commonly sovereign bonds issued by governments considered highly creditworthy in their own currency.

The choice of reference instrument depends first on the currency of analysis. The risk-free rate must be expressed in the same currency as the cash flows. There is no universal risk-free rate; there are as many risk-free rates as currencies. Using a rate in a different currency introduces a fundamental inconsistency. For valuations in euros, practitioners typically use long-term French OATs or German Bunds; for US dollar valuations, US Treasury yields; for Swiss franc valuations, Swiss Confederation bond yields.

Beyond currency, maturity is a second critical parameter. The selected rate should be consistent with the horizon of the cash flows being discounted. In corporate valuation, cash flows often extend over the long term and may include a terminal value. Accordingly, practice generally favors long-term sovereign yields, often the 10-year maturity. Shorter maturities can be justified for finite-life projects or where long-term visibility is structurally limited, but for standard going-concern valuation, a long-term rate better reflects the durable nature of the economic flows.

This choice is not neutral. Short-term rates are more influenced by monetary policy and cyclical conditions, while long-term rates embed expectations of inflation, growth, and sovereign risk over time. Choosing a long-term risk-free rate therefore anchors the cost of capital in a structural perspective consistent with going-concern assumptions.

Expected Market Return (Rm): Definition, Construction, and Estimation Approaches

The expected market return represents the return required by investors to hold a broadly diversified equity portfolio representative of the equity market. It is a central CAPM variable because it is the reference point for systematic risk compensation. Unlike the risk-free rate, the expected market return cannot be observed directly; it is an expectation derived from market data, economic assumptions, and methodological conventions.

Conceptually, the market is treated as an efficient portfolio of all risky assets. In practice, this theoretical portfolio is approximated by broad indices such as the S&P 500 for the United States, the Euro Stoxx for the euro area, or the MSCI World for a global view.

Historically, the most common method has been to use historical index returns as a proxy for expected market returns, assuming that sufficiently long periods provide a reasonable approximation of expectations. This approach typically includes reinvested dividends and can be expressed through arithmetic or geometric averages over decades.

However, historical approaches have a key conceptual weakness: they assume past regimes are representative of future regimes. Interest rates, inflation regimes, sector composition, and monetary policy have changed materially over time. Relying mechanically on historical averages therefore risks projecting the past into the future without explicit adjustment.

To address this, contemporary professional practice increasingly favors forward-looking approaches, deriving the expected market return from current market prices. In this framework, the expected market return is the rate that equates the present value of expected market cash flows with the observed market level. Starting from market capitalization and expected cash flows (dividends and growth), one derives the implied return demanded by investors.

This approach is widely developed by Aswath Damodaran, who regularly computes implied equity returns based on observed valuation levels. In practice, the implied market return is often approximated as the dividend yield plus a sustainable long-term growth assumption consistent with macroeconomic expectations.

Market Risk Premium (Rm − Rf): Equity Risk Compensation and the Core of CAPM

The market risk premium is the additional return investors require to bear equity risk rather than holding a risk-free asset. It is defined as the difference between the expected market return Rm and the risk-free rate Rf. This is not a simple arithmetic spread; it is the quantitative expression of investor risk aversion and equity market uncertainty.

Economically, the market risk premium compensates for systematic risk—the portion of risk that cannot be diversified away. Even a perfectly diversified portfolio remains exposed to macroeconomic shocks, financial cycles, and market-wide confidence shifts. CAPM assumes that only this non-diversifiable risk is remunerated.

Empirically, the market risk premium is not directly observable and must be estimated. Historically, practitioners have used long-term historical equity excess returns as a proxy. More recently, forward-looking approaches estimate an implied premium from current market pricing. In Damodaran’s framework, one estimates the implied market return and subtracts the risk-free rate to isolate the market risk premium, anchoring the premium in current investor expectations rather than in potentially obsolete historical averages.

The market risk premium is the pivot of CAPM: beta has economic meaning only relative to it, because beta measures exposure to this premium. A beta of 1 captures the full premium; higher betas capture more; lower betas capture less.

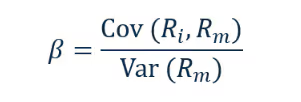

Beta: Systematic Risk Measure and the Link Between Business Risk and Capital Structure

Beta is the central element of CAPM because it links company-specific exposure to the market risk premium. It measures neither total risk nor absolute volatility, but only sensitivity to market movements, i.e., systematic risk—risk that cannot be eliminated through diversification and affects all risky assets simultaneously.

Economically, beta reflects how a company’s performance reacts to economic and financial cycles. Businesses whose results amplify economic fluctuations tend to exhibit betas above 1, while more resilient or defensive activities exhibit betas below 1.

Statistically, beta is defined as a co-movement measure between the asset’s returns and market returns, expressed as the ratio of covariance to market variance:

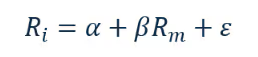

In econometric terms, beta is commonly estimated through a linear regression of the stock’s returns on market returns:

Here, βcaptures sensitivity to the market, while the residual term ε\varepsilonε captures idiosyncratic risk, which is not rewarded under CAPM because it can be diversified away. This statistical formalization underpins CAPM as introduced by William Sharpe (1964).

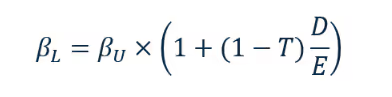

However, observed market betas reflect both business risk and financial leverage. The market beta is therefore a levered beta, influenced by debt. To isolate pure business risk, practitioners use unlevered beta (asset beta). The relationship between levered and unlevered beta is commonly expressed through Hamada’s equation:

where βL is the levered beta, βU is the unlevered beta, D is the market value of debt, E is the market value of equity, and T is the marginal tax rate. The term (1−T) reflects the tax effect of debt, which partially mitigates leverage impact due to interest deductibility.

In valuation practice, the process is typically: estimate levered betas for comparable listed companies, unlever them to extract sector business risk, and then re-lever them to the target company’s capital structure assumptions to obtain a levered beta consistent with the valuation case.

Full Synthesis of the Cost of Equity (Ke): Integrating Rf, Rm, and the Market Risk Premium

The cost of equity represents the minimum return required by shareholders, reflecting the opportunity cost of equity capital and compensation for bearing business and financial risk. Because it is not contractual and not directly observable, it must be estimated through a risk–return framework.

CAPM provides this framework by decomposing required return into a risk-free component and a systematic risk component:

The risk-free rate compensates for time. The market risk premium compensates for bearing equity market risk. Beta scales that premium to the company’s exposure relative to the market. The cost of equity can therefore be understood as an economically coherent combination of time compensation, market risk compensation, and firm-specific systematic exposure.

Cost of Debt (Kd): Credit Risk Compensation and the Financial Translation of External Funding

The cost of debt is the return required by lenders to provide external financing. Debt is contractual and senior in the cash flow waterfall, which reduces lender risk relative to equity and generally results in a lower required return than cost of equity.

Economically, cost of debt compensates for credit risk: the risk the company cannot meet its financial obligations. It depends on business model robustness, cash flow stability, leverage, maturity profile, and macro conditions. When debt is traded, cost of debt can be approximated by yield-to-maturity, reflecting the risk-free rate in the relevant currency plus a credit spread. When debt is not traded, practitioners estimate cost of debt from the risk-free rate plus a credit spread consistent with an implied rating, often inferred from leverage and interest coverage metrics. Damodaran’s mapping between coverage ratios and spreads is frequently used in practice.

A key requirement is to use the marginal cost of debt rather than historical borrowing rates: WACC aims to reflect the opportunity cost of capital today, not past financing conditions.

The Tax Factor (1 − T): The Economic Meaning of Interest Deductibility

The factor (1−T) is often used but frequently misunderstood. It is neither a secondary adjustment nor an accounting correction; it is the direct translation of a structural tax mechanism: interest expense deductibility.

When a company pays interest, that expense reduces taxable income in most jurisdictions, lowering corporate tax paid. The economic cost of debt is therefore not the contractual rate, but the rate net of the tax savings. Multiplying Kd by (1−T) does not change what lenders earn; it reflects what the company effectively bears after the tax shield.

This does not apply to equity because dividends are not tax-deductible at the corporate level. This asymmetry is central to capital structure trade-offs and is consistent with Modigliani and Miller’s 1963 extension incorporating corporate taxes.

WACC Weighting: Capital Structure and the Economic Shares of Invested Capital

WACC does not result from mechanically adding cost of equity and cost of debt; it relies on economic weighting reflecting how the company is financed. Each financing source contributes to overall cost proportionally to its weight in the capital structure, so WACC reflects the aggregated cost of resources used to finance the firm’s assets.

Weights should be based on market values rather than book values, because investors’ required returns relate to economic value at risk. Beyond market values, the key practical question is which capital structure to use. In valuation, WACC should typically reflect a target, sustainable capital structure consistent with long-term operating assumptions, rather than a transitory snapshot.

This target structure may be derived from company history, sector norms, or forward-looking debt capacity analysis. It ensures consistency between long-term business risk and the discount rate applied to long-term cash flows.

WACC Assembly: Bringing the Components Together and Building an Operational Discount Rate

At this stage, all conceptual building blocks have been constructed coherently: cost of equity, after-tax cost of debt, and target capital structure. WACC results from combining them via economic weighting to produce a single rate representing the company’s overall cost of financing.

Formally:

This equation is not a mere identity; it is the synthesis of a structured economic reasoning. E/(D+E) represents the economic share of equity financing, while D/(D+E) represents the economic share of debt financing. The cost of each source is then applied, with the cost of debt adjusted for taxation to reflect its economic net cost.

This is precisely where introducing a WACC calculation table becomes valuable. A well-designed table makes assumptions explicit and traceable, aligns inputs across cost of equity, cost of debt, tax rate and weighting, and allows sensitivities to be run transparently. In professional work, such a table makes the WACC calculation auditable and discussable—an essential feature in valuation, M&A, and fundraising contexts.

Limitations of WACC: A Powerful Tool Under Strict Validity Conditions

WACC is a core corporate finance tool, but it should not be treated as a universal rate applicable indiscriminately. Its relevance depends on implicit assumptions that materially affect decision quality. Understanding limitations does not undermine WACC’s legitimacy; it defines its appropriate scope of use.

A first limitation is WACC’s average, aggregated nature. It assumes that discounted cash flows have a risk profile comparable to the company’s existing business. If a project’s risk differs materially, applying corporate WACC can bias valuation—overstating value for riskier cash flows and understating value for more defensive ones.

A second limitation concerns risk stability over time. WACC is typically applied as a constant rate, yet risk can evolve materially through growth phases, strategic transformations, deleveraging, or turnarounds. A constant discount rate may then fail to reflect the changing risk profile of cash flows.

WACC is also highly sensitive to market assumptions, notably the risk-free rate, market risk premium, and beta. Small changes can materially affect valuation. WACC should be interpreted as a conditional estimate rather than an immutable truth.

Tax integration creates another limitation. The after-tax debt adjustment assumes the firm can effectively benefit from the interest tax shield. If the firm has tax losses, large carryforwards, or uncertain taxable income capacity, the tax shield may be partial, delayed, or uncertain, and applying (1−T) mechanically can overstate the benefit of debt.

Finally, WACC may be insufficient where cash flows display strong optionality or asymmetry, such as innovation projects, sequential investments, or early-stage companies. In such contexts, constant-rate discounting may not capture the value of flexibility, contingent decisions, and alternative future states. WACC remains useful as a first approximation, but may be inadequate as a full representation of economic value.

CEO Statement

WACC is often presented as a technical indicator reserved for valuation specialists or market finance practitioners. In reality, it is a strategic steering tool at the intersection of economic performance, financing, and value creation. When properly understood and applied, WACC helps executives structure investment decisions, arbitrate between growth and profitability, and engage with investors on solid, shared economic foundations.

At Hectelion, we believe the value of a financial tool lies not only in theoretical sophistication, but in its ability to inform decisions. WACC is not an end in itself; it is a decision framework that forces explicit articulation of risk, financing, and market assumptions underlying any growth strategy. This requirement for coherence and transparency is, in our view, what distinguishes rigorous financial analysis from purely mechanical model application.

Conclusion: WACC as a Structuring Framework for Financial Decision-Making

WACC plays a central role in corporate finance because it establishes the fundamental link between risk, return, and value. Behind an apparently simple formula lies a demanding analytical construction combining market assumptions, methodological choices, and professional judgment. A deep understanding of WACC is essential for any serious valuation, M&A process, or investment decision.

This article has shown that WACC is not merely a calculation. It is a structured synthesis of capital providers’ expectations, taxation, and capital structure. Used rigorously, it provides a coherent framework for analyzing value creation. Used without discernment, it can become a source of misinterpretation and poorly calibrated decisions.

Mastering WACC therefore requires both technical understanding of its components and the ability to assess its limitations. It is precisely in this balance—between theoretical rigor and professional judgment—that WACC reveals its full value as a decision-support tool.

Would you like to train in business valuation?

Hectelion offers business valuation training programmes combining rigorous theoretical frameworks, practical methodologies and analysis of real-world cases. These programmes are designed for business leaders, entrepreneurs and finance professionals seeking to strengthen their understanding of valuation mechanisms and secure strategic decision-making.

👉 Learn more about the training

Author

Aristide Ruot, Ph.D.

Founder | Managing Director