Size Premium: WACC and Business Valuation

Size Premium and WACC in Business Valuation: Calculation, Methodology, and Indicative Table

Introduction: Foundations and Stakes of Integrating Size Risk into the WACC

In the context of discounted cash flow (DCF) approaches, the financial valuation of a company relies on a structural variable: the Weighted Average Cost of Capital (WACC). This rate serves as the mechanism for converting future flows into present value and directly influences the resulting valuation level. A marginal variation in the cost of equity can produce a significant effect on the enterprise value, particularly when the flows present a long duration or sustained anticipated growth.

In its standard academic formulation, the cost of equity is determined using the Capital Asset Pricing Model (CAPM), which expresses the return required by investors as a function of the risk-free rate and the market premium adjusted by the beta. However, this model is based on the hypothesis of an efficient and diversified market, in which only systematic risk is compensated. This theoretical construction raises a difficulty when transposed to small and medium-sized enterprises (SMEs), particularly private ones, whose structural characteristics differ significantly from the large capitalizations observed on organized markets.

It is in this context that the notion of the size premium intervenes. It designates the additional return historically observed or required to compensate for the additional risk associated with small-capitalization companies. The empirical existence of a size effect was documented by Rolf W. Banz (1981), who highlighted an inverse relationship between market capitalization and the average return on stocks. This anomaly was later integrated into the multi-factor model developed by Eugene F. Fama and Kenneth R. French (1992), through the SMB (Small Minus Big) factor, confirming that size constitutes an additional explanatory factor for returns.

On a professional level, the main risk premium databases, notably those published by Kroll, present increasing premiums as capitalization decreases. Nevertheless, these estimates rely exclusively on listed companies. However, even the smallest companies in these deciles display capitalizations far higher than those of the majority of private SMEs. This asymmetry raises a question of methodological transposability.

A study published in The Journal of Entrepreneurial Finance in 2025 shows that the relationship between size and premium follows a strongly non-linear logarithmic dynamic, with a rapid increase in the required additional return at the lowest levels of capitalization (pp. 33–41). The author also emphasizes that the mechanical use of the lowest deciles from listed markets leads to an underestimation of the risk of truly small companies.

Consequently, several questions arise. Should the size premium be systematically integrated into the WACC in the context of an SME valuation? Are data from listed markets adapted to private companies? Is there a risk of double counting with the specific premium? And above all, according to what rigorous method should one proceed in order to maintain the economic consistency of the discount rate?

The present article proposes to analyze these questions in a structured manner. After having examined the academic and empirical origin of the size premium, we will specify its economic definition and theoretical foundations. We will then analyze the situations in which its integration into the WACC is justified, the financial reasons advocating for its use, as well as the technical modalities of application. A numerical example will illustrate its impact on valuation, before presenting an updated table of observable premiums and concluding with an argued methodological position.

The stake is clear: integrating size risk must neither be an automatic process nor a purely conventional practice, but a rigorous analysis based on identifiable data and overall financial consistency.

Academic and Empirical Origin of the Size Premium

The size premium finds its origin in empirical work conducted on the US financial markets at the turn of the 1980s. At that time, the dominant theory of the Capital Asset Pricing Model (CAPM), developed notably by William F. Sharpe (1964) and John Lintner (1965), postulates that only systematic risk — measured by the beta — explains the expected return of an asset. Within this theoretical framework, a company’s market capitalization should not constitute an independent explanatory factor for return.

This prediction was, however, challenged by the founding study by Rolf W. Banz published in 1981 in the Journal of Financial Economics. Banz highlighted a statistically significant relationship between the size of listed companies and their risk-adjusted returns. Small-cap companies displayed, over a long period, average returns superior to those of large caps, even after controlling for the beta. This anomaly, designated by the term Small Firm Effect, suggests that the CAPM, in its single-factor version, is incomplete. Size seems to capture a dimension of risk not integrated into the classic measure of market risk.

This intuition was further developed and formalized by Eugene F. Fama and Kenneth R. French in their 1992 article published in the Journal of Finance. The authors introduced a three-factor model integrating, alongside the market factor, a value factor (HML – High Minus Low) and a size factor (SMB – Small Minus Big). The SMB factor measures the average outperformance of small caps relative to large caps, confirming that size constitutes a systematic determinant of observed returns.

Since this foundational work, the size effect has been the subject of nourished academic debates. Some studies in the 1990s suggested a temporary weakening of the anomaly in more efficient markets. However, subsequent research demonstrates that the effect persists, notably in micro-cap segments or when controlling for biases related to company quality. Thus, Clifford S. Asness et al. (2018) show that the size effect remains statistically significant when adjusted for "junk" companies, i.e., those of low fundamental quality.

While academic work established the empirical existence of the size effect, its operational diffusion in valuation practice owes much to the work of Roger G. Ibbotson. Through the annual Stocks, Bonds, Bills and Inflation (SBBI Yearbook) publications, developed within Ibbotson Associates, the author systematized the historical analysis of returns by capitalization deciles.

This approach allowed for the transformation of an academic anomaly into a tool directly exploitable by practitioners. The size premiums from the SBBI Yearbooks were progressively integrated into so-called "build-up" approaches for the cost of equity, notably in valuations of SMEs and private companies.

This methodology was then adopted and enriched by professional databases developed by Duff & Phelps, today integrated within Kroll. These publications present size premiums calculated from market capitalization deciles and now constitute a structural reference in audit firms, investment banks, and independent expert reports.

It is, however, necessary to emphasize an essential methodological limit: all of this work relies exclusively on listed companies, benefiting from observable liquidity, standardized regulatory transparency, and access to financial markets. The mechanical extension of these premiums to private companies, often of much smaller size, raises a question of external validity.

In this regard, a recent contribution provides a decisive insight. The study by Craig S. Galbraith (2025), based on more than 2,000 transactions of private companies from the DealStats database, confirms that the relationship between size and risk premium follows a non-linear logarithmic function, with a marked accentuation at the lowest levels of capitalization (pp. 33–41). The results show that using the lowest deciles from listed markets leads to a significant underestimation of the risk of truly small companies.

Historically, the size premium thus appears as the product of a double dynamic:

- An empirical anomaly highlighted by academic research in market finance;

- A progressive methodological formalization carried out by valuation practitioners.

This double lineage — scientific and professional — explains both its importance in the construction of the cost of capital and the persistent debates relative to its scope of application and its modalities of integration into the WACC.

Economic Definition and Conceptual Scope of the Size Premium

The size premium can be defined as the additional return required by investors to compensate for the additional risk associated with low-capitalization companies. It constitutes an adjustment to the cost of equity aimed at reflecting structural characteristics that are not fully captured by systematic risk alone, as measured by the beta.

From a conceptual point of view, the size premium is not an autonomous factor in the strict sense of the original CAPM. It proceeds from an empirical observation: at comparable market risk, small caps have historically generated returns superior to large caps. This outperformance is interpreted as the remuneration for an additional risk that the single-factor model does not explicitly model.

On an economic level, several mechanisms can explain this increased return requirement.

Firstly, small companies generally present limited operational diversification. Their dependence on a restricted number of clients, suppliers, or geographic markets increases the sensitivity of their flows to specific shocks. This concentration increases the anticipated volatility of results.

Secondly, the liquidity of the security or investment is often reduced. In listed markets, small caps present higher bid-ask spreads and lower trading volumes. In the case of private companies, illiquidity is structural: the investor does not benefit from an organized secondary market allowing for a quick exit. This constraint justifies an additional return requirement.

Thirdly, small structures generally have more limited bargaining power with their economic partners. Literature in industrial organization shows that large companies benefit from economies of scale and increased market power, favorably influencing their margins and the stability of their flows. Conversely, small entities bear a more marked competitive risk.

Fourthly, information asymmetry is more pronounced. Large listed companies are followed by financial analysts, audited according to strict standards, and subject to regulatory transparency obligations. Private SMEs do not benefit from the same level of informational coverage, which increases the uncertainty perceived by investors.

It is important to distinguish the size premium from other adjustments frequently encountered in valuation.The company specific risk premium aims to reflect risks proper to the analyzed company: managerial dependence, extreme concentration, litigation, temporary financial fragility. The size premium, for its part, corresponds to a structural and transversal risk related to the capitalization segment.

Similarly, the illiquidity discount applied in certain asset-based approaches or in valuations of minority stakes pursues a distinct objective: it aims to adjust the value obtained to account for the absence of a secondary market. The size premium intervenes upstream, in the determination of the cost of equity.

Thus defined, the size premium constitutes a macro-structural adjustment tool for the discount rate. It does not reflect a one-off or idiosyncratic risk, but a statistically observed characteristic of the small-capitalization segment.

It is part of both an academic tradition and a professional construction:

- It corrects a limit of the CAPM in its strictly single-factor version;

- It reflects an observable economic reality relative to the risk profile of small structures.

The central question is therefore not to know if the size premium exists — empirical literature confirms its existence — but how to interpret it correctly and integrate it consistently into the construction of the WACC, without redundancy or over-adjustment.

Would you like to have your business valued?

Hectelion conducts independent valuations in France and Switzerland — business sale, divorce, shareholders agreement, taxation.

→ Book a call — 30 minutes, confidential

Conditions for Integrating the Size Premium into the WACC

The integration of the size premium into the weighted average cost of capital cannot be automatic. It assumes a prior analysis of the economic structure of the evaluated company, its financing environment, and the chosen discounting method. In practice, the question is not so much to know if the size premium exists — its empirical existence is documented — as to determine in what circumstances its integration into the cost of equity is economically justified.

In the first place, the size premium finds its full relevance when the evaluated company presents an economic capitalization significantly lower than the thresholds observed in listed markets, including in the lowest deciles published by Kroll. In the case of private SMEs, notably family-owned or entrepreneurial ones, the value of equity can be at levels very distant from the segments analyzed in databases derived from public markets. The study by Craig S. Galbraith (2025) shows precisely that, for companies of very low capitalization, the premium grows logarithmically and significantly exceeds the levels observed in the 10z deciles of professional databases (pp. 39–41). The mechanical application of premiums from listed markets then leads to an underestimation of risk.

In the second place, the integration of the size premium is particularly relevant when the company presents a high structural concentration. Dependence on a limited number of clients or suppliers, marked sectoral exposure, or low geographic diversification reinforces the potential volatility of flows. In this context, size acts as an amplifier of global economic risk.

In the third place, the size premium is necessary when access to capital markets is restricted. Small structures generally have more limited bargaining power vis-à-vis financial institutions, suffer a higher financing cost, and present a reduced shock absorption capacity. These elements directly influence the cost of equity required by a rational investor.

On the other hand, certain situations can lead to relativizing, or even excluding, the application of a distinct size premium. When the company belongs to a diversified group, benefits from significant financial strength, or operates in a contractual environment stabilized by secured multi-year commitments, isolated size may not constitute an autonomous risk factor. Similarly, if a substantial specific premium is already integrated into the cost of equity to reflect idiosyncratic risks, an additional adjustment for size could lead to a redundancy phenomenon.

It is also appropriate to distinguish valuation approaches. In a DCF method based on a WACC, the size premium intervenes at the level of the cost of equity. In contrast, in an approach by multiples of strictly comparable transactions, the size effect may already be implicitly integrated into the observed multiples, provided the quality and relevance of the selected comparables are high. A consistent analysis then assumes avoiding any double counting.

Finally, the temporality of risk must be taken into consideration. The size premium is justified when the structural characteristics related to the company's dimension are durable. If significant growth is anticipated in the short term and substantially modifies the capitalization profile, dynamic modeling of the cost of equity may prove more appropriate than a static adjustment.

Ultimately, the integration of the size premium into the WACC stems from a methodological decision based on an argued economic analysis. It must neither be systematic nor excluded by principle. Its relevance depends on the capitalization segment, the operational risk profile, and the overall consistency of the chosen valuation model.

Economic Foundations Justifying the Integration of the Size Premium

The integration of the size premium into the weighted average cost of capital does not constitute a simple statistical adjustment derived from historical observations. It relies on identifiable economic foundations that reflect a structural reality proper to small-scale companies. Understanding these mechanisms is essential in order to avoid a mechanical application and to anchor the adjustment in a consistent financial logic.

The first foundation lies in the increased economic vulnerability of small structures. A small-sized company generally presents limited diversification of its flows. Dependence on a restricted number of clients or major contracts increases the anticipated volatility of results. This concentration increases the risk of future flow disruption and justifies a higher return requirement from investors.

The second foundation relates to market power and economies of scale. Large companies often benefit from a structural advantage in their relations with suppliers and distributors. Industrial organization literature highlights the existence of asymmetric bargaining power favoring large-scale actors. Conversely, small entities bear a more pronounced competitive risk, increased pressure on margins, and a more limited shock absorption capacity.

The third explanatory element concerns the liquidity and transferability of the investment. In listed markets, small-cap securities generally present lower trading volumes and higher spreads. In the case of private companies, illiquidity is structural. The investor does not benefit from an organized secondary market allowing for a quick or low-cost exit. This constraint increases the return requirement and reinforces the economic justification for an additional premium.

A fourth factor relates to information asymmetry. Large listed companies are subject to strict regulatory obligations, recurring audits, and significant analyst coverage. Private SMEs present a lower level of transparency, heterogeneous information quality, and sometimes concentrated governance. Informational uncertainty increases perceived risk and translates into a surcharge on the cost of equity.

Finally, the limited financial flexibility of small companies constitutes a determining element. Their access to external financing is often more restricted and more costly. In a situation of economic tension, their capacity to raise capital or refinance their debt can be compromised, which increases the overall risk borne by shareholders.

These different elements show that the size premium does not correspond solely to a statistical anomaly observed on the stock markets. It reflects a combination of structural factors affecting the stability, liquidity, and resilience of future flows.

However, the integration of this premium must be carried out with discernment. When the mentioned characteristics are already taken into account by a substantial specific premium or by prudent flow modeling, an additional adjustment could lead to an overvaluation of risk. The internal consistency of the valuation model remains paramount.

To conclude, the integration of the size premium finds its legitimacy in tangible economic mechanisms. It constitutes a methodological response to a structurally distinct risk profile proper to small-capitalization companies. The following section will analyze the technical modalities of integration.

Modalities of Integration of the Size Premium into the WACC

The integration of the size premium into the weighted average cost of capital assumes a rigorous articulation between financial theory and valuation practice. It intervenes exclusively at the level of the cost of equity, and not at the level of the cost of debt. Its impact on the WACC is indirect but mechanically significant.

In a strict academic framework based on the CAPM, the cost of equity is determined according to the following relationship:

where Rf represents the risk-free rate, Rm−Rf the market premium, and β the systematic sensitivity of the security to the market.

However, this model does not explicitly account for the size factor when applied to private companies. In practice, professionals resort to a so-called build-up approach, consisting of adding different risk components in order to more faithfully reflect the economic profile of the evaluated company.

In this framework, the cost of equity can be formulated as follows:

The size premium thus inserts itself as an autonomous component of the cost of equity, just like the specific risk premium. It modifies neither the risk-free rate nor the market premium but constitutes an additional adjustment intended to reflect the capitalization segment of the company.

An alternative consists of integrating the size premium into a multi-factor model, such as the Eugene F. Fama and Kenneth R. French model, in which the SMB factor is explicitly modeled. However, this approach remains difficult to operationalize for private companies due to the lack of observable market data. This is why the additive method remains predominant in practice.

Once the cost of equity is adjusted, the WACC is determined according to the classic formula:

where E represents the value of equity, D financial debt, Kd the cost of debt, and T the tax rate.

The addition of a size premium increases Ke, which raises the WACC, all else being equal. The effect on the valuation obtained by discounting flows is therefore direct: an increase in the discount rate leads to a decrease in enterprise value.

It is, nevertheless, appropriate to avoid any methodological inconsistency. The size premium must not lead to a double accounting of risk. If the beta used comes from a sample of comparable small-capitalization companies, part of the size effect may already be integrated into the systematic risk measurement. Similarly, a significant specific premium could already reflect certain structural risks related to the company's dimension.

The internal consistency of the model therefore imposes:

- A documented justification of the source of the selected size premium;

- A verification of the absence of redundancy with other adjustments;

- A sensitivity analysis in order to measure the impact on the final value.

In reality, the integration of the size premium into the WACC relies on an additive and structured logic. It constitutes an adjustment to the cost of equity intended to reflect a structural risk not entirely captured by standard models. Its implementation requires rigor, traceability of hypotheses, and global consistency of the chosen valuation framework.

Determination and Calculation of the Size Premium

The determination of the size premium constitutes a central step in the construction of the cost of equity. It must rely on an identifiable, documented methodology consistent with the chosen valuation model. Several approaches coexist in practice: historical empirical, application by published deciles, or econometric modeling.

Before examining these methods, it is appropriate to specify the main concepts used.

Definition of Terms

In order to avoid any methodological ambiguity, the following terms are employed in the developments that follow:

- Capitalization (Equity Value): Market value of the company's equity. In the case of a private company, it corresponds to the estimated value of the equity within the framework of the valuation.

- Risk-free rate (Rf): Return on an asset considered free of default risk, generally a long-maturity government bond.

- Market Premium (Equity Risk Premium): Historical differential between the average return of the stock market and the risk-free rate.

- Beta (β): Measure of the sensitivity of an asset's return relative to variations in the global market.

- Size Premium: Additional return required to compensate for the structural risk associated with low-capitalization companies.

- SMB (Small Minus Big): Factor introduced by Eugene F. Fama and Kenneth R. French measuring the average outperformance of small caps relative to large caps.

- Rsmall: Average return (historical or expected) of a representative portfolio of small caps, used to empirically measure the size effect.

- Rmarket: Average return (historical or expected) of the global stock market, serving as a reference in the calculation of the size premium.

- a: Constant (intercept) of an econometric regression model relating the size premium to capitalization. It represents the estimated premium level when ln(Equity Value)=0, i.e., when the size variable equals 1 in the chosen unit.

- b: Sensitivity coefficient (slope) of the econometric model. When negative, it reflects a decrease in the premium as capitalization increases.

- ln(Equity Value): Natural logarithm of the value of equity. This transformation allows for modeling a non-linear relationship between size and premium, generally more realistic for small capitalizations.

Empirical Approach Based on Historical Returns

The empirical approach constitutes the original academic foundation of the size premium. It relies on the statistical observation that small-capitalization companies have historically generated returns superior to those of large caps, at comparable market risk.

This anomaly was highlighted by Rolf W. Banz (1981), then formalized in the multi-factor framework by Eugene F. Fama and Kenneth R. French (1992). The SMB (Small Minus Big) factor measures precisely this performance differential between small and large cap portfolios.

In its simplest form, the empirical size premium is expressed as:

where:

- Rsmall corresponds to the historical average return of a portfolio of small caps;

- Rmarket corresponds to the historical average return of the global market.

In the strict framework of the Fama-French model, the SMB factor is written as:

where Rbig represents the average return of a portfolio of large caps.

Operational Methodology

To estimate the size premium according to this approach, it is appropriate to:

- Constitute or select a database of stock returns sufficiently long (generally 20 to 50 years);

- Segment the companies into homogeneous capitalization groups;

- Calculate the annual average returns of each segment;

- Measure the differential between small caps and the market (or large caps).

Returns can be calculated as an arithmetic average (more suited for an annual projection) or a geometric average (more consistent over long cumulative periods). The methodological difference can produce significant gaps in the final estimation.

This approach presents a strong academic robustness. It relies on observable and measurable data and is part of financial market theory.

However, it presents two major limits when applied to private SMEs:

- Firstly, it requires market data, which do not exist for private companies.

- Secondly, the "small cap" portfolios used in historical studies still correspond to capitalizations often well above those of very small enterprises.

Thus, if the empirical approach conceptually founds the size premium, its direct application remains essentially relevant for listed markets. For private SMEs, it must be adapted or supplemented by practical or econometric methods, developed in the following sections.

Practical Approach by Capitalization Deciles

In the professional practice of valuation, the size premium is most often determined from premium tables by capitalization segments. This approach was popularized by the work of Roger G. Ibbotson via the SBBI Yearbooks, then widely institutionalized in the frameworks of Duff & Phelps, today integrated at Kroll. The principle consists of measuring, over a long period, the historical outperformance of small-cap portfolios relative to the market, then presenting this differential in the form of premiums classified by capitalization deciles (or sub-deciles).

On an operational level, the method proceeds in three steps. First, the evaluator estimates the equity value of the company or a reasonable approximation of its economic size. Second, they identify the capitalization category closest in the chosen framework (decile, sub-decile, or bracket). Finally, they apply the corresponding size premium as an additive component of the cost of equity.

This approach presents a determining advantage: it is standardized, traceable, and reproducible, which explains its diffusion in Big4 environments, investment banks, and judicial expert reports. It nevertheless includes a major methodological limit when transposed to private SMEs: even the weakest segments of databases derived from listed markets often remain structurally higher than the implicit capitalization of many private companies. Galbraith's study highlights precisely this point, recalling that the smallest category of listed firms remains of an order of magnitude far superior to that of typical private companies, which can lead to an underestimation of the premium truly required for the smallest structures (pp. 33–35).

Logarithmic Econometric Approach

In order to overcome the granularity limits of decile tables, an econometric approach consists of modeling the premium as a continuous function of size. The empirical results of Galbraith (2025), based on transactions of private companies (DealStats), show that the relationship between size and premium is non-linear and is more adequately expressed via a logarithmic function (pp. 39–41).

The generic formulation is as follows:

where a is the constant, b the sensitivity coefficient (negative in the presented estimations), and ln(Equity Value) the natural logarithm of the value of equity. The economic reading is direct: as the company grows, the premium decreases, but at a decreasing rate (concave form), which reflects an acceleration of the premium in very low capitalizations.

In the smoothed model presented by Galbraith, the estimated coefficients lead to an equation of the type:

These parameters are the result of a statistical estimation on a given scope (country, period, sectors), and must therefore be used with caution: they do not constitute a "universal norm," but an estimation function allowing for the production of a consistent premium when listed deciles do not correctly cover the observed size of the evaluated company (Table 5, pp. 40–41).

This approach brings two operational benefits: it produces a continuous premium (no threshold effect between deciles) and it is particularly adapted to micro-capitalizations, where the size effect becomes the most discriminating.

Full Calculation Example

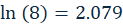

In order to concretely illustrate the determination and integration of the size premium in a Swiss context, let us consider a private company whose equity value is estimated at CHF 8 million.

This capitalization typically corresponds to an established, profitable, and structured Swiss SME, but remains far below the capitalizations observed in the weakest segments of international listed markets.

The econometric model presented previously is as follows:

The value of equity must be expressed in millions, in the same unit as that used during the estimation ,Equity Value = 8

Calculation of the natural logarithm:

Application of the equation:

The estimated size premium therefore amounts to 4.9%.

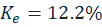

Suppose the following parameters, consistent with a Swiss environment:

- Risk-free rate (Confederation 10-year): 1.25%

- Swiss market premium: 5.50%

- Adjusted beta: 1.10

The cost of equity becomes:

Without size premium:

The integration of the size premium thus increases the cost of equity by about 5 points.

Suppose a target structure typical of a Swiss SME:

- 65% Equity

- 35% Debt

With:

- Cost of debt Kd = 3.5%

- Effective tax rate T = 15% (average cantonal approximation)

The WACC is established as follows:

Without the size premium, the WACC would have been close to 6%.In this realistic case for a Swiss SME:

- The size premium significantly increases the cost of equity;

- It raises the WACC by about 3 points;

- It mechanically reduces the enterprise value obtained by DCF.

Even at CHF 8 million of capitalization, the size effect remains structural. It is therefore not a marginal adjustment, but a parameter that can significantly modify the valuation.

Indicative Size Premiums for Private SMEs: Application of an International Transactional Model (2025)

The table below represents size premiums calculated from a logarithmic model estimated on a sample of private company transactions from the DealStats database, as published by Craig S. Galbraith (2025).

The model relies on the relationship:

where the coefficients a and b come from an econometric estimation based on predominantly American transactions.

Reminder of the model:

The premiums presented below thus constitute an indicative proxy for SMEs operating in developed markets, including Switzerland and France. They do not constitute official national tables.

Capitalization thresholds are rounded to facilitate reading. The presented premiums do not constitute a normative recommendation but a methodological illustration.

CEO Statement

"The size premium regularly sparks debates between academic approach and professional practice. In theoretical models, it finds its origin in the empirical work of Rolf W. Banz and in the multi-factor formalization of Eugene F. Fama and Kenneth R. French. In professional frameworks, it has been structured through the successive publications of Roger G. Ibbotson, then integrated into practices disseminated by Duff & Phelps and today Kroll.

However, the size premium must never be applied mechanically. It constitutes neither a universal constant nor a standardized percentage. It is the expression of a real economic risk: reduced liquidity, managerial dependence, limited access to financing, commercial concentration, non-institutionalized governance.

In 2025, Hectelion was mandated for the valuation of a Swiss family business whose equity value was between CHF 4 and 7 million. The in-depth analysis of the risk profile led to retaining a size premium between 6% and 9%, validated following an independent review by an expert auditor. This range exceeded the levels resulting from a strict reading of listed deciles, but reflected the specific economic reality of the evaluated company.

This experience confirms a strong methodological conviction: whenever possible, the evaluator should calculate the size premium themselves, provided they have the financial tools, the relevant databases, and the necessary financial engineering skills. Adapted econometric modeling, sectoral transactional analysis, or consistent logarithmic calibration allow for a finer approach to the company's real structural risk, rather than limiting oneself to an automatic application of standard tables.

The objective is not to artificially increase the discount rate, but to ensure that the cost of capital faithfully reflects the risk assumed by the investor. An underestimation leads to an excessive valuation; an overestimation destroys economic value.

The determination of the size premium thus constitutes an exercise in balance between academic rigor, compliance with professional practices, and concrete economic analysis of the case.

At Hectelion, we consider that the WACC must never be the result of an automatic process, but that of a structured, documented, and defensible reasoning."

Get a first indicative estimate

Hectelion offers a free indicative valuation tool based on Franco-Swiss market data — no commitment required.

→ Access the indicative valuation tool

Conclusion: A Structural Variable of the Cost of Capital

The size premium constitutes neither a marginal anomaly nor a simple accessory adjustment to the cost of equity. It is at the very heart of the determination of the return required by the investor and, by extension, of the construction of the WACC.

The founding work of Rolf W. Banz and the multi-factor formalization of Eugene F. Fama and Kenneth R. French established the empirical existence of a robust size effect. The professional frameworks developed by Roger G. Ibbotson, then integrated into practices disseminated by Duff & Phelps and today Kroll, allowed for its operationalization.

However, the mechanical transposition of deciles from listed markets to private SMEs remains insufficient when one descends to the lowest levels of capitalization. Recent literature on private transactions reminds us that the relationship between size and premium follows a non-linear dynamic, with an accentuation of risk at the most reduced levels.

The determination of the size premium therefore requires:

- An identifiable methodological base;

- Consistency with the chosen model (adjusted CAPM or build-up);

- A documented economic justification;

- A sensitivity analysis on the final valuation.

In practice, a gap of a few percentage points in the size premium can significantly modify the enterprise value obtained by discounting flows. It influences not only the cost of equity but also the WACC and, in fine, the negotiation between investors and shareholders.

The size premium must not be perceived as a normative parameter, but as the quantitative translation of a structural risk proper to small economic dimension companies.

In terms of valuation, rigor does not consist of applying a standard percentage, but of demonstrating that the chosen rate faithfully reflects the economic reality of the analyzed company.

Interested in Business Valuation Training?

Hectelion offers professional training in business valuation, combining theoretical frameworks, practical methodologies, and real-world case studies.

👉 Learn more about our valuation training programs

Author

Aristide Ruot, Ph.D.

Founder & Managing Director