Online business valuation simulator: estimate your value and audit your EBITDA

A free, confidential online simulator that audits your EBITDA and estimates your company's value using market multiples.

Introduction: how much is your company really worth, and how to find out in minutes

Every business owner asks the question one day, often at night, sometimes the evening before a meeting with a buyer or an investor: how much is my company worth? Most online calculators answer with a single figure, drawn from a simple percentage of turnover, without looking at real profitability, at debt, or at the sector. It is reassuring and wrong. A serious valuation is an estimate framed by standards, not a magic number, and it is expressed as a range, never to the last cent.

« Market value is the estimated amount for which an asset or liability should exchange on the valuation date between a willing buyer and a willing seller in an arm's length transaction, after proper marketing and where the parties had each acted knowledgeably, prudently and without compulsion. », International Valuation Standards Council (IVSC).

Three reasons make the subject pressing in 2026. First, the mergers and acquisitions market is rebounding strongly, and an owner who is approached wants a reliable first estimate before opening any discussion. Second, market data and artificial intelligence now allow a value to be estimated online, free of charge and in a few minutes, without disclosing one's accounts to an intermediary. Third, the quality of the EBITDA and net debt, two parameters that simplistic calculators ignore, alone determine half of the gap between a credible estimate and an illusion. This article presents Hectelion's Acontos simulator, explains how it works, how and by whom it was built, how to read its report, what happens to your data, why it differs from a classic calculator, its advantages and its limits, five mistakes to avoid, two figured franco-Swiss cases and ten key questions.

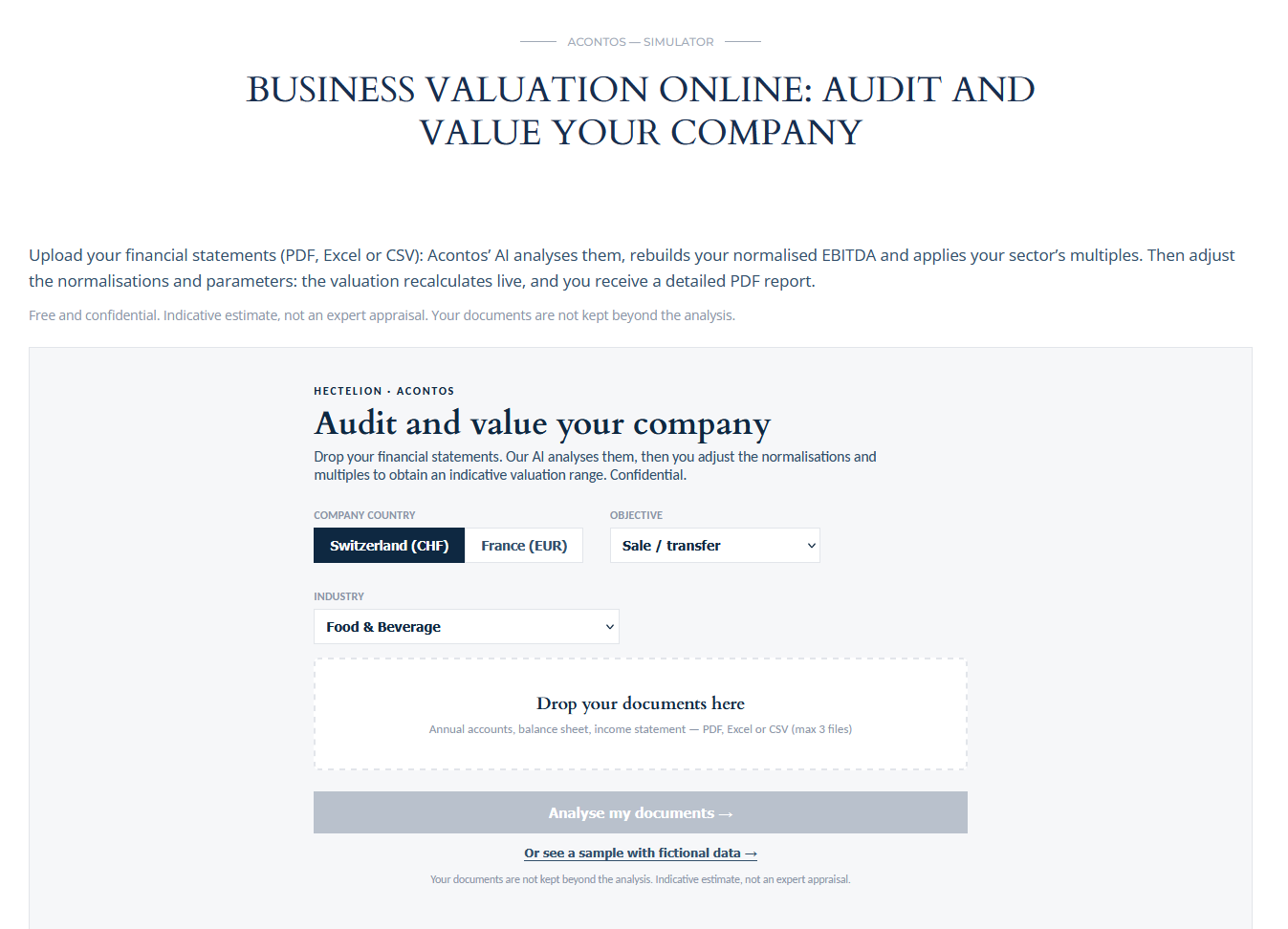

Estimate the value of your company online, free of charge and in confidence

The Acontos simulator audits your EBITDA and estimates the value of your company from your accounts, using market methods, and returns an indicative PDF report.

Launch the valuation simulator, it is free and confidential.

To go further than an indicative estimate, book thirty minutes with Hectelion and have a documented multi-method valuation established by our business valuation service.

Definition: what is an online business valuation simulator?

An online business valuation simulator is a tool that, from your financial statements, applies recognised valuation methods to deliver an indicative value range. It is neither a judicial appraisal, nor a formal enforceable valuation report, but a first, fast and educational measure of what the company is worth on the market. Hectelion's Acontos simulator goes further than a classic calculator: it does not merely apply a multiple to turnover, it rebuilds the enterprise value then the equity value, taking into account normalised profitability and debt.

The difference lies in the method. Where a mass-market calculator returns a single figure, a real simulator reasons like a valuer: it normalises the EBITDA, applies several sector multiples drawn from real transactions, distinguishes enterprise value from equity value, and shows an assumed range. This is the logic set out in our reference publication on how much a business is worth, transposed into an interactive tool available online.

Origin: from bespoke valuation to AI-assisted online estimation

For a long time, knowing the value of one's company meant engaging a firm, waiting several weeks and paying several thousand francs for a report. This barrier kept most SME owners away from a simple first estimate, even though they needed it to decide, negotiate or reassure themselves. The democratisation of market data, then the arrival of artificial intelligence models able to read annual accounts, changed the game.

The Acontos simulator was born of this observation. It combines two building blocks: a base of sector multiples built on real transactions and listed comparables observed by Hectelion between 2023 and 2025, and an automated extraction of accounts assisted by an artificial intelligence model, which turns a PDF balance sheet into structured data. The owner thus obtains in a few minutes what once required a back-and-forth of several weeks, without giving up the rigour of a multi-method approach aligned with IVSC standards.

Why use a valuation simulator before any step

First, to obtain a credible first estimate. Before engaging an adviser or answering a buyer, an owner needs a defensible order of magnitude, not a figure produced by a back-of-the-envelope calculation. Second, to prepare an operation: a sale, a fundraising, the entry of a partner or a family transfer all start with a question of value. Third, to understand one's levers: the simulator shows where value is created, between the quality of the EBITDA, the sector multiple and net debt.

Fourth, to preserve confidentiality. Testing a value online, without handing one's accounts to an intermediary or exposing oneself on the market, is a decisive advantage for a cautious owner. Fifth, to save time and money: the estimate is free, immediate and confidential, where a formal valuation has a cost and a lead time. The simulator does not replace that formal valuation, it prepares it and helps decide whether to go further.

How the Acontos simulator works, step by step

The method reproduces, in a guided way, the reasoning of a valuer. First, the owner uploads one to three accounting documents, balance sheet and income statement, in PDF, Excel or CSV format, and specifies the country and the objective of the exercise. Second, an artificial intelligence model reads these documents and extracts the structured financial data, turnover, EBITDA, debt, cash, over one or several financial years.

Third, the simulator carries out the audit and normalisation of the EBITDA: it isolates the restatements, above-market owner remuneration, non-recurring charges, exceptional items, and flags the share of the normalised EBITDA that rests on restatements still to be substantiated. This is a point that classic calculators ignore entirely, even though it conditions the soundness of the whole valuation. Fourth, it applies several sector multiples, transactional by country and listed European, drawn from real data, to compute an enterprise value range.

Fifth, it builds the net debt bridge: the equity value, the one the seller actually receives, equals the enterprise value less net debt. Sixth, it enriches the reading with the implied multiple, the leverage level, the financeability of a debt-funded buyout and a read by buyer type, financial or strategic. The owner finally receives an indicative PDF report, together with a written summary, after entering an email address.

How the Acontos simulator was built, and by whom

The Acontos simulator is not a generic product bought off the shelf, it is the translation into a tool of a valuation firm's know-how. Its extraction block relies on the Claude Sonnet 5 artificial intelligence engine, developed by Anthropic, able to read a balance sheet and an income statement in PDF format and to return the structured financial data, turnover, EBITDA, debt, cash, in a few seconds. Where a classic form imposes tedious and error-prone manual entry, artificial intelligence does the reading work of an analyst, without copying errors, and leaves the owner to check and adjust the values before any calculation.

But an extraction engine does not make a valuation. The whole method was designed and calibrated by Aristide Ruot, Ph.D., founder and managing director of Hectelion: the choice of the real sector multiples observed between 2023 and 2025, the logic of normalising the EBITDA and identifying the share to substantiate, the net debt bridge, the read by buyer type, and above all the safeguards, a range rather than a single figure, a systematic reminder of the indicative and non-enforceable nature. Artificial intelligence speeds up and secures the data entry, human expertise frames the reasoning and sets its limits. It is this combination, a state-of-the-art AI engine at the service of a franco-Swiss valuer's methodology aligned with IVSC standards, that distinguishes Acontos from a mere online calculator.

How to read your valuation report

The report does not come down to a figure, it is read in blocks. At the top sits the enterprise value range and, above all, the equity value range, the one that actually returns to the seller once net debt is deducted. Then comes your company's implied multiple, positioned against the sector benchmarks, transactional and listed, to know whether you sit above or below your market. The report also indicates the quality of the EBITDA, with the share of restatements still to be substantiated, the leverage level and a read by buyer type, financial or strategic.

Each block calls for an action. The equity value range frames your price expectation, never to be read to the last cent, because it is an interval, not an amount. The implied multiple against the sector median tells you whether your valuation is stretched or cautious. The share to substantiate flags what must be documented before opening a negotiation, on pain of seeing the value melt away in due diligence. Leverage and financeability measure a buyer's ability to fund the operation with debt. Finally, the read by buyer orients your strategy, aiming for a fund at a market price or an industrial buyer willing to pay a synergy premium. Well read, the report is not an answer, it is a map.

Data privacy and processing: what happens to your balance sheet

An owner's first hesitation, before even testing a simulator, is legitimate, handing over one's accounts. Acontos's answer is clear. The documents you upload are never stored. They pass through memory for the time of the extraction, a few seconds, then disappear, no balance sheet and no income statement is kept, neither on a server nor in a database. The processing is moreover hosted in Europe, on an infrastructure located in Paris.

A second guarantee, artificial intelligence is not trained on your data. The Claude Sonnet 5 engine reads your accounts to extract the figures, but this information does not serve to train the model, in accordance with the policy of Anthropic's commercial programming interface. Your data feeds no learning and is reused for nothing other than your own estimate.

A third point, transparency on what is kept. Only the information you provide voluntarily is retained, your email address and your contact details, together with the figured summary of your estimate, for the sole purpose of sending you the report and, if you wish, exchanging afterwards. Nothing is resold, nothing is passed to a third party. This approach respects the principles of the GDPR, data minimisation, a clear purpose, and a right of access and erasure on first request. Testing your value with Acontos means doing it in confidence.

When to use the valuation simulator

The simulator applies first ahead of a sale reflection: even before contacting an adviser, it gives the owner the order of magnitude that frames the discussion and avoids starting on an unrealistic expectation, too high or too low. It is also useful before a fundraising or the entry of an investor, to objectify the pre-money value and not to suffer the range imposed by the other party. It also sheds light on a family transfer, a management buyout or the arbitration between several scenarios.

Conversely, the simulator is not suitable when an enforceable figure is required: litigation, divorce, judicial appraisal, an operation on listed securities, regulated information. In these cases, only a formal valuation, documented and signed, holds up, and one must then call on an independent expert. The right reflex is to use the simulator to decide, then to move to the formal valuation when the stakes justify it.

Which sectors and which company sizes are covered

The simulator covers thirteen sectors, chosen to represent the fabric of franco-Swiss SMEs, food and agriculture, automotive, transport and logistics, wholesale trade, construction, software development, distribution, e-commerce, hospitality and tourism, industry and production, media, marketing and communication, business services, healthcare and pharmaceuticals, and IT services. For each, the simulator mobilises transactional multiples specific to the country, France or Switzerland, and listed European comparables, because the same business is not valued at the same price on either side of the border.

On the size side, the tool is designed for SMEs and mid-caps, in line with Hectelion's scope of work, operations of 2 to 500 MCHF. It assumes a profitable company, whose EBITDA can be normalised, because that is the raw material of multiple-based valuation. For an early-stage company, without a positive EBITDA, other approaches are more suitable, such as those described in our publication on startup valuation. The simulator therefore targets established companies, those for which a reading through profitability makes sense.

Who to turn to for a reliable online estimate

Not all simulators are equal, and three criteria separate a credible tool from a gadget. The first is the origin of the multiples: an estimate is only worth something if the multiples applied come from real transactions and comparables, not from fanciful averages. The second is the method: normalisation of the EBITDA, distinction between enterprise value and equity value, a range rather than a single figure, are the marks of a valuer's reasoning. The third is the backing of a real firm, able to take over if the owner wants to go further.

The Acontos simulator brings together these three qualities because it is developed and fed by Hectelion, an independent boutique firm with dual franco-Swiss expertise and economic independence from traditional financial intermediaries. Its multiples come from transactions and listed comparables actually observed, its method is aligned with IVSC standards and AMF and SIX market practice, and the owner can, at any time, switch to M&A support or a formal valuation. Hectelion is not FINMA-authorised and does not act on listed-company operations.

Advantages: free, fast and confidential

The first advantage is that it is free: the estimate costs nothing, where a formal valuation has a price. The second is speed: a few minutes are enough, from uploading the accounts to the PDF report, against several weeks for a full appraisal. The third is confidentiality: the owner tests their value without exposing themselves on the market or handing their accounts to an intermediary, a major asset in a reflection phase.

To these benefits is added the educational dimension. The report is not limited to a figure: it explains the quality of the EBITDA, the positioning of the multiple against the sector, the financial structure and the read by buyer type. The owner does not leave only with a range, they leave with an understanding of the levers that move it, which is precisely what they need to prepare the next step.

Limits: indicative, data-dependent and non-enforceable

The first limit is the indicative nature: the simulator delivers an estimate, not a formal valuation, and its result has no enforceable value before a judge, a shareholder or the tax authority. The second is the dependence on the data entered: an estimate is only worth what the uploaded accounts are worth, and a poorly normalised EBITDA or an omitted debt distorts the whole range. The third is the absence of qualitative context: dependence on a client, quality of management, key contracts, litigation, all elements that a simulator does not capture and that a real due diligence reveals.

These limits are not defects, they are the normal boundaries of the exercise. The Acontos simulator assumes them explicitly: the result is an indicative estimate, neither investment advice, nor an appraisal, and Hectelion is not subject to FINMA. When the stakes go beyond the simple first estimate, the handover to a documented multi-method valuation and a financial due diligence becomes indispensable.

After the simulator: from an indicative estimate to a formal valuation

The simulator is a first step, never a point of arrival. As soon as an operation takes shape, a sale, a fundraising, the entry of an investor or a transfer, one must move from an indicative estimate to a formal valuation, multi-method, with discounted cash flows, multiples and an asset-based approach crossed, documented assumptions and a signed, enforceable report. It is this rigour that holds up before a buyer, their advisers, the tax authority or a judge, where a simulator range cannot.

This is precisely Hectelion's role. The firm takes over with a documented business valuation, a financial due diligence, the financial structuring of the operation and merger and acquisition support, with dual franco-Swiss expertise and independence from traditional financial intermediaries. The simulator qualifies the need, the team turns it into a result. Book thirty minutes to discuss it.

The 5 mistakes to avoid

Mistake 1: confusing an indicative estimate with a formal valuation

A simulator range orients a reflection, it does not found a transaction nor stand against a third party. Taking it for a firm price leads to rigid expectations and negotiations that derail. The estimate prepares the decision, the formal valuation secures it, and confusing the two is the first source of disillusion.

Mistake 2: neglecting the normalisation of the EBITDA

Applying a multiple to a raw accounting EBITDA, without restating owner remuneration, non-recurring charges and exceptional items, gives a value that is either inflated or understated. The normalisation of the EBITDA is the foundation of any multiple-based valuation, and the share of restatements to substantiate must always be identified.

Mistake 3: forgetting net debt

Enterprise value is not equity value. What the seller receives is enterprise value less net debt. Confusing the two, as most simplistic calculators do, leads to announcing a price that does not exist and to discovering the gap at the worst moment, in the middle of a negotiation.

Mistake 4: relying on a single multiple

A single multiple, chosen at random or drawn from a national average, produces false precision. A serious valuation crosses several approaches, transactional and listed, by sector and by country, and shows a range. A figure that is too neat is almost always a wrong figure.

Mistake 5: using a simulator without real market data

Most free calculators apply generic ratios disconnected from the field. Without multiples drawn from real transactions and comparables, the estimate has no footing. The value of a simulator rests first on the quality and freshness of the market data that feeds it, sector by sector and country by country.

Case 1: online estimate of a French IT services SME

A French IT services SME generates 4.3M EUR of turnover and an accounting EBITDA of 560,000 EUR. The simulator normalises this result by adding back 90,000 EUR of restatements, mainly above-market owner remuneration and a few non-recurring charges, for a normalised EBITDA of 650,000 EUR. It flags, however, that about 55,000 EUR of these restatements remain to be substantiated, i.e. nearly 400,000 EUR of value exposed as long as the supporting documents are not produced.

By applying the real transactional multiple of the IT services sector in France, in the region of 7.2 to 7.3 times the EBITDA, the simulator obtains an enterprise value of 4.68 to 4.75M EUR. After deducting net debt of 900,000 EUR, the equity value comes out between 3.78 and 3.85M EUR. The report adds that leverage, at 1.4 times the EBITDA, leaves good debt capacity for a buyer, which makes the deal financeable with debt. This range is not a price, it is a documented starting point for the negotiation.

Case 2: online estimate of a Swiss industrial SME

A Swiss industrial SME generates 8 MCHF of turnover and an accounting EBITDA of 1.10 MCHF. After normalisation, adding back 150,000 CHF of restatements of which 40,000 CHF still to be substantiated, the normalised EBITDA settles at 1.25 MCHF. The simulator applies the real transactional multiple of industry in Switzerland, in the region of 5.3 to 5.5 times the EBITDA, and obtains an enterprise value of 6.6 to 6.9 MCHF, brought down to an equity value of 4.8 to 5.1 MCHF after net debt of 1.8 MCHF.

The report enriches the reading. The listed European benchmark for the sector, higher, at 6.7 to 7.3 times the EBITDA, places the value a strategic buyer might aim for, up to 8.4 to 9.1 MCHF, by paying a synergy premium. With leverage of 1.4 times the EBITDA, the company remains financeable within a debt-structured buyout. The owner thus has, in a few minutes, a range by buyer type, a solid base before engaging a real process.

A word from the founder

« I built this simulator because too many owners navigate blind on the value of their company. A calculator that multiplies turnover by a percentage is not an estimate, it is a lottery draw. We deserve better. »

« What I wanted was to put in the hands of an owner the reasoning we apply in the firm: normalise the EBITDA, apply real multiples, distinguish enterprise value from what they actually receive, and always speak in a range. Free of charge, in confidence, in a few minutes. »

« The simulator does not replace a formal valuation, and it does not claim to. It is a first step, honest and serious. Those who want to go further know where to find us, and those who just want to understand leave with a real understanding of their value. »

Aristide Ruot, Founder and Managing Director of Hectelion SA.

FAQ: the 10 essential questions on the valuation simulator

Introduction: what to keep in mind before the questions

The Acontos simulator delivers an indicative estimate of a company's value, from its accounts, using market methods. The answers below clarify how it works, its data, its reliability, its confidentiality and the boundary with a formal valuation.

Q1: Is the valuation simulator really free?

Yes, the estimate and the indicative PDF report are free. The owner uploads their accounts, obtains a value range and a summary, at no cost. Only a formal valuation, more thorough and documented, is then subject to a quote.

Q2: Is my accounting data confidential?

Yes, completely. The uploaded documents are never stored, they pass through memory for the time of the extraction then disappear, and artificial intelligence is not trained on your data. Only your email and the figured summary of the estimate are kept to send you the report. The dedicated confidentiality chapter details this GDPR-compliant processing.

Q3: What data are the multiples based on?

On real transactions and listed comparables observed by Hectelion between 2023 and 2025, broken down by sector and by country for the transactional, at European scale for the listed. These are not generic averages but market benchmarks kept up to date.

Q4: What does the EBITDA audit change to the estimate?

Everything. A raw accounting EBITDA does not reflect real profitability. The simulator normalises it by restating owner remuneration, non-recurring charges and exceptional items, then flags the share of restatements to substantiate. It is this normalised profitability that serves as the base for the multiple.

Q5: Why a range rather than a single figure?

Because a value is an estimate, not a certainty. Crossing several multiples, transactional and listed, produces a range that faithfully conveys the uncertainty. A single figure gives false precision and turns against whoever announces it at the first contradiction.

Q6: Does the simulator replace a valuation by an expert?

No. It delivers an indicative estimate, useful to decide and prepare, but without enforceable value. For litigation, a real operation or regulated information, a documented and signed formal valuation is required. The simulator prepares this step, it does not replace it.

Q7: Which documents must be uploaded?

One to three accounting documents, balance sheet and income statement, in PDF, Excel or CSV format, over one or several financial years. The more complete and recent the accounts, the more reliable the estimate. Artificial intelligence extracts the necessary financial data automatically.

Q8: Is artificial intelligence reliable for reading my accounts?

The model extracts the structured data from the uploaded documents, turnover, EBITDA, debt, cash, which the user can check and adjust in the simulator before the calculation. AI speeds up the data entry, but the owner keeps control of the assumptions.

Q9: Does the simulator work for France and Switzerland?

Yes. The owner specifies the country, and the simulator applies the corresponding transactional multiples, France or Switzerland, as well as listed European comparables. The tool is bilingual and designed for the franco-Swiss reality of SMEs, in EUR as in CHF.

Q10: What to do with the report once obtained?

It serves as a basis for reflection and discussion: understanding your value, identifying your levers, framing an expectation before a sale or a fundraising. If a real operation is needed, the next step is a formal valuation and support, which Hectelion provides in full independence.

Conclusion: a serious first step towards the value of your company

Estimating the value of one's company should neither cost a fortune, nor take weeks, nor rest on a simplistic calculation. The Acontos simulator brings a third way: an online estimate, free and confidential, but built with the rigour of a valuation firm, an audit of the EBITDA, real market multiples, the net debt bridge and a read by buyer type. The owner obtains in a few minutes a defensible range and, above all, an understanding of what moves it.

What remains is the right place of the tool. It prepares, it enlightens, it decides whether to go further, but it does not replace a formal valuation when the stakes require it. That is where the value of a simulator backed by a real franco-Swiss firm lies: offering an honest first step, then, for those who want it, the handover of a documented and independent expertise.

Summary of the article

Hectelion's Acontos simulator estimates online the value of a company from its accounts, free of charge and in confidence, with an indicative PDF report. It differs from a classic calculator by its method: extraction of the accounts assisted by artificial intelligence, audit and normalisation of the EBITDA with identification of the share to substantiate, application of real transactional and listed sector multiples, then passage from enterprise value to equity value via net debt.

The tool reasons like a valuer: it shows a range rather than a single figure, computes the implied multiple and leverage, assesses debt financeability and reads value by buyer type, financial or strategic. Its advantages are that it is free, fast, confidential and educational; its limits are the indicative nature, the dependence on the data entered and the absence of enforceable scope.

The two cases, a French IT services SME valued between 3.78 and 3.85M EUR of equity and a Swiss industrial SME between 4.8 and 5.1 MCHF, show the way forward: normalise the EBITDA, apply real multiples, deduct net debt and reason in a range. The simulator is a serious first step; the formal valuation and the support take over when the operation becomes real.

Sources

- Anthropic, Claude Sonnet 5 model for financial data extraction

- Aswath Damodaran (NYU Stern), valuation multiples and the role of EBITDA

- Autorité des Marchés Financiers (AMF), financial information and business valuation

- Bpifrance Création, estimating the value of a business for sale

- Conseil Supérieur de l'Ordre des Experts-Comptables (France), business valuation work

- International Valuation Standards Council (IVSC), international valuation standards

- SECA, Swiss Private Equity and Corporate Finance Association, valuation and transaction practices in Switzerland

- Swiss Federal Tax Administration (FTA), practitioners' method for valuing unlisted securities

Author

Aristide Ruot, Ph.D.

Founder | Managing Director, Hectelion SA