Business Valuation: Approaches, Methods and Valuation Techniques

Business Valuation: Approaches, Methods and Mechanisms for Determining Company Value

Introduction: Business Valuation, Between Financial Science and Economic Judgment

Business valuation is one of the most demanding exercises in modern finance. It cannot be reduced to a mechanical calculation or the automatic application of a standardized formula. It lies at the intersection of economic theory, financial modeling, and strategic analysis. The intrinsic difficulty of the exercise stems from the fact that we seek to assign a present value to a set of uncertain future cash flows, in an economic environment that is inherently unstable.

From the early twentieth century, Irving Fisher, in The Theory of Interest (1930), established the fundamental principle that the value of an asset corresponds to the present value of the future income it generates. This founding principle still structures today’s discounted cash flow approach.

Modern finance subsequently consolidated this intuition. The work of Franco Modigliani and Merton Miller (1958, 1963) shows that, in a theoretical world without taxes or transaction costs, a firm’s value depends on its earning capacity rather than on its financing structure. Although idealized, this proposition remains a cornerstone of the contemporary understanding of the cost of capital.

Later, Aswath Damodaran, professor at NYU Stern School of Business, synthesized contemporary practice by stating that valuation is “the bridge between the numbers and the strategic story” (Valuation: Tools and Techniques for Determining the Value of Any Asset, 2012).

Thus, business valuation is not limited to a financial projection. It requires:

- An understanding of the business model;

- An assessment of risk;

- A methodological selection adapted to the context;

- A critical analysis of the assumptions adopted.

The central issue can be formulated as follows: how can one estimate, in a rigorous and defensible manner, the economic value of a business in an uncertain environment, taking into account both past performance, future prospects, and market conditions?

This article adopts a structured approach. It first retraces the academic and empirical origins of valuation, then clarifies the fundamental concepts before presenting the different methodological approaches and their practical implications.

Would you like to sell, acquire or have your business valued?

Hectelion handles all these operations in France and Switzerland — business sale, acquisition, divorce, shareholders agreement, taxation, assets and financial instruments.

→ Book a call — 30 minutes, confidential

Academic and Empirical Origins of Business Valuation

Business valuation does not arise from a single model or an isolated theoretical construction. It is part of a gradual evolution of economic thought, which began well before the emergence of contemporary financial models. As early as the eighteenth century, Adam Smith, in An Inquiry into the Nature and Causes of the Wealth of Nations (1776), distinguished between value in use and value in exchange, laying the conceptual foundations for thinking about price formation and the economic value of productive assets. At that time, the firm was not yet understood as an autonomous financial entity, but rather as a set of factors of production organized to generate wealth and profit.

In the nineteenth century and the early twentieth century, in a context dominated by patrimonial and inheritance logics, a firm’s value was essentially assimilated to the value of its net assets. The accounting approach prevailed: the balance sheet was the central reference, and the firm was seen as an aggregate of tangible goods that could be liquidated or transferred. This patrimonial conception corresponded to an economy still largely industrial, where tangible assets—land, machinery, inventories—represented the core of wealth. Valuation was then static and retrospective; it measured what was owned, not what would be produced.

A major turning point occurred with the emergence of intertemporal analysis and the formalization of reasoning in terms of future cash flows. Irving Fisher, in The Theory of Interest (1930), argued that the value of an asset corresponds to the discounted sum of the income it is likely to generate in the future. This idea introduced a fundamental break: value ceased to be exclusively linked to the stock of assets and became forward-looking and dependent on economic expectations. The firm was now viewed as a mechanism generating monetary flows, and discounting became the central conceptual tool for measuring value.

The post-war period marked the advent of modern finance. The work of Franco Modigliani and Merton Miller (1958) shows that, in a frictionless theoretical world, a firm’s value depends on its earning capacity rather than its financing structure. This proposition underpins contemporary analysis of the cost of capital and structures the distinction between enterprise value and equity value. In parallel, modern portfolio theory developed by Harry Markowitz (1952), followed by the Capital Asset Pricing Model by William Sharpe (1964), introduced a formal measure of systematic risk and made it possible to estimate the return required by investors. Valuation thus became embedded in a mathematically structured framework explicitly integrating the risk–return trade-off.

Alongside these academic developments, financial market practice and merger-and-acquisition activity gave rise to an empirical approach based on comparison. Observing stock market transactions and disposals led to the use of multiples—price/earnings ratios, EBITDA multiples, revenue multiples—as indicators of relative valuation. This comparative method, born from practice before being theorized, was gradually structured in professional manuals, notably by Shannon Pratt and Roger Grabowski, who systematized the articulation between market data and financial methodology. Valuation thus became an exercise combining intrinsic modeling and reference to observed prices.

Finally, recent decades have enriched valuation by integrating uncertainty and strategic flexibility. The work of Black and Scholes (1973), then Cox, Ross, and Rubinstein (1979), on the valuation of financial options opened the way to the analysis of real options applied to investment decisions. The firm is no longer evaluated solely as a deterministic sequence of cash flows, but as a portfolio of adaptive strategic choices. At the same time, globalization of markets, the rise of intangible assets, and international normative frameworks—notably IAS 36 on impairment testing—have reinforced methodological rigor and transparency of assumptions. Contemporary valuation thus appears as the outcome of a historical construction combining a patrimonial approach, forward-looking cash flow analysis, market referencing, and probabilistic integration of risk.

Definition of Business Valuation

Business valuation can be defined as the methodological process aimed at estimating, at a given date, the economic value of an entity in consideration of its ability to generate future cash flows, the nature of its assets, and the level of risk associated with its activity. It is not an absolute or intangible measure, but a structured estimate based on explicit and consistent assumptions. As Aswath Damodaran emphasizes, valuation is inseparable from assumptions about growth, profitability, and risk; it is a rational and reasoned construction rather than an intrinsic truth.

It is necessary from the outset to distinguish value from price. Value corresponds to a theoretical estimate derived from financial reasoning; price is the result of a concrete transaction between parties with specific objectives, information, and constraints. This distinction is essential in mergers and acquisitions, where strategic factors—synergies, bargaining power, financing constraints—can lead to a price above or below so-called intrinsic value. The work of Koller, Goedhart, and Wessels reminds us that intrinsic value is a rational benchmark, while price reflects market conditions and the specific expectations of the parties.

Valuation also requires a conceptual distinction between enterprise value and equity value. Enterprise value measures the overall value of operating assets independent of their financing; equity value corresponds to the residual portion attributable to shareholders after deducting net debt. This articulation follows directly from Modigliani and Miller’s work, which clarified the relationship between capital structure and economic value creation.

Beyond these distinctions, valuation rests on a fundamental principle: a company’s value is a function of the economic flows it will generate for its capital providers, discounted at a rate reflecting their level of risk. This principle, inherited from Irving Fisher, underpins the modern forward-looking approach. However, this definition is not limited to cash flow discounting: it also incorporates the value of identifiable assets, competitive dynamics, sector outlook, and, where applicable, the strategic options embedded in the business model.

In professional practice, valuation is always contextualized. It varies depending on whether it is carried out for transactional, tax, accounting, or judicial purposes. International standards, notably IAS 36, frame certain valuations by requiring impairment tests based on recoverable amount, defined as the higher of value in use and fair value less costs of disposal. This normative dimension reminds us that valuation is not only a theoretical exercise but also a regulated process when conducted within an accounting or prudential framework.

Finally, business valuation must be understood as a probabilistic rather than a deterministic exercise. It does not lead to a single, immutable number, but to a range of values resulting from scenarios, assumptions, and sensitivities. Methodological rigor requires transparency of assumptions, internal consistency of models, and the cross-checking of results obtained through different approaches. In this sense, valuation is both a scientific discipline grounded in modern finance and an exercise of professional judgment mobilizing experience, prudence, and strategic analysis.

When Should a Business Valuation Be Performed?

A business valuation becomes necessary whenever a decision involves an economic trade-off regarding property rights, a transfer of ownership, or a reorganization of capital. It arises whenever it is appropriate to determine, in a structured and reasoned manner, the value of an asset or entity in a context where interests may diverge. Valuation thus serves as a rational arbitration tool among stakeholders—shareholders, investors, executives, creditors—by providing an objectified analytical framework.

The most emblematic context remains mergers and acquisitions. In a sale or acquisition, valuation helps establish an economically coherent value range, serving as a basis for arbitration between estimated intrinsic value and the price actually negotiated. This process frames transactional discussions and distinguishes what is attributable to the company’s own economic performance from what stems from strategic logic or buyer-specific synergies. As Koller, Goedhart, and Wessels remind us, intrinsic value is an indispensable reference point to structure negotiation (Valuation: Measuring and Managing the Value of Companies, Wiley, 2020).

Fundraising and financial restructurings also involve a delicate trade-off between dilution and financing growth. Determining pre-money or post-money valuation conditions the future distribution of capital and the balance of economic rights. In this context, valuation helps reduce the information asymmetry described by Akerlof (1970) and makes it possible to set estimation bounds within which negotiation between investors and founders can occur. It becomes a balancing tool between risk-taking and the expected remuneration of capital.

Patrimonial or contentious situations also require an independent arbitration framework. Business transfers, inheritance, divorce, or partner buyouts require a fair estimate based on recognized and defensible methods. The aim here is not to maximize price, but to establish a reasonable value enabling dispute resolution or objective allocation of economic rights. Valuation plays a central role in legal security and in preventing subsequent challenges.

Valuation is also required in a constraining normative framework. International standards, notably IAS 36 – Impairment of Assets, require impairment tests based on recoverable amounts calculated using rigorous financial methods. In these situations, valuation becomes an accounting arbitration tool between book value and estimated economic value, ensuring the reliability of published financial information.

Beyond exceptional events, valuation can be part of ongoing governance. It enables arbitration between investment projects, assessment of value creation or destruction relative to the cost of capital, and guidance of long-term strategic decisions. From this perspective, valuation becomes a permanent tool for optimal resource allocation, structuring managerial choices within an economically coherent value range.

Below is a non-exhaustive list of key contexts in which a business valuation is required or strongly recommended:

- Mergers and acquisitions (buy-side / sell-side),

- Fundraising,

- Capital reorganization,

- Transfer and succession,

- Disputes and judicial arbitration,

- Contributions in kind / structuring legal transactions,

- Impairment tests and accounting obligations,

- Valuation of specific assets,

- Internal strategic arbitration,

- Tax optimization and international structuring,

- Incentive plans and management packages,

- Performance steering and measurement of value creation.

Get a first indicative business estimate

Hectelion offers a free indicative valuation tool based on Franco-Swiss market data — no commitment required.

→ Access the indicative valuation tool

Why Perform a Business Valuation

Business valuation does not respond only to a technical requirement; above all, it is a decision-support tool designed to clarify an economic arbitration. Determining the value of a company means objectifying its ability to generate future cash flows in a given environment, taking into account the risk borne by capital providers. Valuation thus replaces intuition or subjective perception with a structured analysis based on explicit and verifiable assumptions.

In a transactional context, valuation serves to frame negotiation and reduce information asymmetry between parties. It helps identify an economically coherent value range from which price discussions can proceed. As Koller, Goedhart, and Wessels point out, intrinsic value is an indispensable analytical reference, even if the final price incorporates strategic or competitive considerations (Valuation: Measuring and Managing the Value of Companies, Wiley, 2020). Valuation then becomes an instrument of financial discipline, preventing decisions from being driven solely by emotional or speculative dynamics.

Beyond negotiation, valuation makes it possible to measure value creation or destruction. From a governance perspective, it provides a synthetic indicator of economic performance by comparing the return generated by the firm to the cost of capital employed. This logic, developed notably around the concept of Economic Value Added by Stewart (The Quest for Value, 1991), highlights that growth creates value only if it exceeds the cost of the resources mobilized. Valuation thus becomes a strategic steering tool rather than a one-off exercise.

It also plays a role in legal and regulatory security. In operations framed by accounting or tax standards, valuation helps justify the amounts adopted and ensure compliance with applicable standards. IAS 36 impairment tests, for example, require a rigorous estimate of recoverable amounts to ensure the reliability of published financial information. Valuation thus contributes to the credibility of financial statements and investor confidence.

In patrimonial or contentious contexts, valuation helps establish an equitable arbitration basis between parties. It helps prevent conflicts by objectifying the economic value of rights held. This fairness dimension is essential in family transfers, partner restructurings, or judicial expert reports, where methodological neutrality is a core requirement.

Valuation also serves a forward-looking function. It forces management to formalize assumptions about growth, profitability, and risk, and to confront these projections with a structured financial discipline. In this sense, valuation is a strategic anticipation tool: it assesses the sustainability of a business model, identifies value-creation levers, and frames capital allocation decisions within coherent estimation bounds. It is therefore a fundamental instrument of modern governance.

Who Should Be Mandated to Perform a Business Valuation?

Choosing the practitioner responsible for a business valuation is itself a strategic trade-off. Valuation is not a simple technical exercise that can be mechanically replicated; it involves structuring assumptions, risk assessment, and a nuanced understanding of the economic and legal context. The credibility of the outcome therefore depends on the evaluator’s technical competence, independence, and ability to justify conclusions methodologically.

Several categories of players operate in the valuation market. Large international audit and consulting firms have specialized transaction services and valuation departments, particularly active in IFRS contexts, impairment testing, or complex transactions. Their strength lies in standardized methods, deep databases, and institutional recognition. However, these organizations often operate within a highly formalized normative framework, primarily oriented toward accounting or large-scale transactional requirements.

Investment banks and M&A advisors also perform valuations, generally within the logic of a competitive process. Their analysis is market-driven and negotiation-oriented, integrating transaction comparables and strategic considerations. In this context, valuation is a tool serving a specific transaction and sits within a broader sell-side or buy-side mandate.

Court experts and independent specialists mainly intervene in contentious, inheritance, or arbitration contexts. Their mission requires strict impartiality and the production of a technically defensible report before a judicial or administrative authority. Methodological robustness and transparency of assumptions are then decisive.

Alongside these institutional actors, independent corporate finance boutiques such as Hectelion occupy a strategically relevant intermediate position for business owners and shareholders. They combine rigorous academic expertise, concrete transaction experience, and operational agility—often decisive in contexts where responsiveness and personalization are essential. Their capital independence and absence of structural conflicts of interest constitute a key advantage, especially when valuation must serve as a basis for delicate arbitration among partners, investors, or strategic counterparts.

Unlike large investment banks or international audit firms, independent boutiques are often led by entrepreneurs who themselves have an operational understanding of the challenges faced by the companies they advise. This cultural proximity to management fosters a finer reading of sector dynamics, financing constraints, and the strategic trade-offs specific to SMEs, mid-caps, or family-owned businesses. Valuation is then not treated as a standardized exercise, but as a strategic diagnostic embedded in a broader vision of development or transfer.

In this framework, a dedicated corporate finance, M&A, and valuation firm—integrating demanding methodology, European sector databases, comparative transaction analysis, and advanced analytical tools—can offer a balance between technical depth and tailored analysis. For companies that do not require the intervention of a heavy international structure, this model provides access to an equivalent level of expertise with a cost structure generally more suited to the size and stakes of the engagement. The issue is not only budgetary; it also lies in the quality of the strategic dialogue between the evaluator and management.

Ultimately, the choice of evaluator must be consistent with the objective pursued: regulatory requirement, transactional negotiation, patrimonial arbitration, or strategic steering. Independence, technical competence, the ability to explain assumptions, and the ability to present a reasoned value range are the key selection criteria. Since valuation is grounded as much in scientific rigor as in professional judgment, the practitioner must be able to articulate method, prudence, and sector understanding.

How to Perform a Business Valuation

Every business valuation begins with a precise analysis of the context in which the evaluator is mandated. This context forms the methodological foundation of the entire work: it defines the purpose of the valuation, the chosen scope, the structuring assumptions, and the level of prudence required. A valuation performed in the context of an M&A transaction will not be conducted in the same way as a valuation for tax or inheritance purposes. In a transactional environment, the evaluator must incorporate the consequences of a potential change of control, the departure of the executive, the cost of replacing them, and the potential impact on revenue or the stability of commercial relationships. In many cases, a financial due diligence-type analysis even precedes the valuation exercise in order to identify necessary adjustments. Conversely, in a going-concern framework—for example in a tax context where management and organization remain unchanged—assumptions rest on a more pronounced structural stability.

After this in-depth understanding of the context, the evaluator builds a valuation model based on recognized methods to measure, quantify, and assess the indicative value of the company and its equity. Not all methods are systematically applied; they must be chosen with discernment, consistency, and suitability to the mandate. Certain approaches may prove inappropriate given the nature of the activity or the quality of available information. In practice, the inadequacy of a method often becomes apparent de facto when results deviate materially from observable economic realities.

In building this model, the evaluator must incorporate economic parameters specific to the sector, competition, and market in which the company operates. Competitive environment, business cyclicality, capital intensity, or dependence on certain customers or suppliers directly influence the assessment of residual risk. These factors can justify an increase or decrease in estimated equity value. Valuation cannot therefore be purely mechanical; it must reflect the economic and strategic reality of the relevant sector.

The evaluator also performs sensitivity analyses. Using analytical tables and parametric simulations, they explore different assumptions regarding the discount rate, growth, or profitability in order to navigate within coherent value zones. This approach identifies the most determining variables and frames the uncertainty inherent in any financial projection. The objective is not to produce an isolated number, but to determine reasoned valuation bounds.

At the end of this analytical phase, the evaluator drafts a report containing a synthesis of the indicative value of the company, equity value, and, where applicable, value per share or unit. This draft is presented to the client, who can then discuss with the evaluator to clarify assumptions, understand results, and highlight any additional elements likely to influence the analysis. This exchange phase is essential: it ensures mutual understanding and data coherence.

After this final meeting and the integration of any justified adjustments, the evaluator delivers the final report. It formalizes, in a structured manner, the chosen methodology, applied assumptions, performed analyses, and reached conclusions. The valuation then becomes a reference document designed to support a strategic, patrimonial, or transactional decision in a transparent and professional framework.

Difference Between “Evaluation” and “Valuation” of a Business

In everyday business language, the terms “evaluation” and “valuation” are often used interchangeably. Yet a conceptual distinction should be made to avoid methodological confusion. “Evaluation” refers to the structured and reasoned process aimed at estimating the economic value of a business at a given date, within a determined context. It implies a complete analytical approach, integrating understanding of the engagement, selection of methods, analysis of assumptions, and determination of coherent estimation bounds. It therefore constitutes a comprehensive discipline.

“Valuation,” by contrast, more specifically refers to the application of a tool or method used to determine an indicative value. For example, discounting future cash flows, applying a sector multiple, or reconstructing adjusted net asset value are valuation techniques. They are instruments serving the evaluation process, but cannot replace it. In other words, valuation is a means; evaluation is the structured process that frames and justifies the use of those means.

This distinction is particularly important in transactional environments. It is common to hear that a business “is worth eight times EBITDA” or “is worth ten million,” whereas this is in fact a point valuation obtained by applying a market ratio. Without analyzing context, specific risks, and necessary adjustments, such an approach remains incomplete. Evaluation, on the other hand, requires the comparison of several methods, critical analysis of observed gaps, and justification of the assumptions retained.

From an academic standpoint, the notion of intrinsic value, developed notably in modern finance literature, refers to an estimate grounded in the company’s economic fundamentals. Valuation is the technical tool enabling one to approximate this intrinsic value. Damodaran’s work reminds us that every estimate depends on assumptions and that process rigor is decisive for credibility (Investment Valuation, Wiley, 2012). The quality of an evaluation thus depends less on model sophistication than on the overall coherence of the approach.

In professional practice, maintaining this distinction avoids analytical shortcuts. An isolated valuation may produce a number, but only a complete evaluation can explain that number, measure its sensitivity, and assess its relevance in the specific context of the engagement. This approach is particularly crucial when the estimate must serve as a basis for strategic or patrimonial arbitration.

Valuation is a technical tool; evaluation is a methodological discipline integrating analysis, judgment, and coherence. Distinguishing these two notions is not a semantic subtlety, but a professional requirement aimed at ensuring the solidity and transparency of the value estimation process.

The Main Approaches and Methods for Business Valuation in an Evaluation Engagement

Business evaluation relies on a set of major approaches recognized by financial doctrine and professional practice. These approaches do not oppose one another; they complement each other and make it possible to confront different readings of an entity’s economic value. Classically, the literature distinguishes the cost-based or asset-based approach, the market approach, the income approach, and, in certain specific contexts, the real options approach. Each rests on a distinct conceptual logic and fits specific economic situations.

The cost-based approach originates from the patrimonial conception of value. It consists of estimating the value of a company from its net assets (NAV), potentially adjusted (Adjusted NAV) and substantial value to reflect their true economic value. This method remains relevant in contexts where value lies mainly in held assets—real estate companies, asset holding companies, or businesses in liquidation. It reflects a relatively static view of value, centered on assets rather than future earning capacity.

The market approach is based on comparison. It consists of observing valuations of comparable businesses, either listed on the stock exchange or acquired in recent transactions. The underlying assumption is that businesses with similar characteristics should be valued using similar ratios. This approach is widely used in transactional practice, notably to assess the coherence of an estimate derived from other methods. It reflects the collective perception of investors at a given point in time.

The income approach is the foundation of modern finance. It rests on the principle that a company’s value corresponds to the present value of future cash flows it will generate for its capital providers, in line with Irving Fisher (1930) and subsequent developments in financial theory. This approach is particularly suited to operating businesses whose value depends primarily on earning capacity and growth trajectory. It explicitly integrates time and risk.

In addition to these three main approaches, the real options approach, derived from the valuation theory of financial options developed by Black and Scholes (1973) and extended by Cox, Ross, and Rubinstein (1979), allows strategic flexibility and future managerial choices to be incorporated into value estimates, especially in innovative or highly uncertain sectors. This approach is more complex and is used only in specific contexts where value partly lies in the ability to adapt strategy.

In practice, none of these approaches can, in isolation, claim to perfectly reflect economic reality. The evaluator must select the most relevant methods given the engagement context and confront the results to determine a coherent value range. The complementarity of approaches provides methodological robustness, avoiding excessive dependence on a single estimation model.

The Cost Approach: Net Asset Value (NAV), Adjusted Net Asset Value (Adjusted NAV) and Substantial Value

The cost approach is grounded in an asset-based rationale according to which the value of a company corresponds to the economic value of its assets less its liabilities. Historically, it reflects a static conception of value, focused on the assets held rather than on the future earning capacity of the business. Although modern finance generally favors forward-looking approaches, the asset-based method remains relevant in specific contexts, particularly where value primarily resides in tangible assets or where the valuation is conducted from a liquidation or patrimonial perspective.

Approach Based on the Net Asset Value (NAV)

Net Asset Value (NAV) represents the simplest form of the asset-based approach. It corresponds to shareholders’ equity as reported in the balance sheet, that is, the difference between total recorded assets and total liabilities. In other words, NAV is strictly equal to the book value of shareholders’ equity. This equivalence allows the valuator to immediately verify the consistency of the calculation by reconciling it with the equity amount disclosed on the balance sheet. Formally, it may be expressed as follows:

NAV = Total accounting assets – Total accounting liabilities = Book shareholders’ equity

In its logic, this method relies exclusively on data derived from historical financial statements. It assumes that the company’s value is reflected by its balance sheet as presented, without specific adjustments. NAV is therefore a retrospective measure based on applicable accounting standards, whether national or international. From a methodological standpoint, reconciling the arithmetic computation with published equity constitutes a basic consistency check.

Let us consider a simplified example. A company reports total assets of CHF 5,000,000 and total liabilities of CHF 3,500,000. The Net Asset Value therefore amounts to CHF 1,500,000, which must correspond to the shareholders’ equity disclosed in the balance sheet. If the company has 150,000 shares outstanding, the book value per share is CHF 10. This calculation illustrates both the operational simplicity of the method and the ease with which it can be internally verified.

However, this simplicity also constitutes its primary limitation. Net Asset Value reflects historical values, often depreciated under prudent accounting rules that may significantly diverge from actual economic values. Fixed assets may be understated if they have appreciated in value, particularly in the case of real estate. Conversely, certain assets may be overstated if their market value has declined. Furthermore, NAV does not capture unrecorded intangible assets such as brand recognition, customer relationships or know-how.

From a methodological perspective, NAV offers the advantage of objectivity, traceability and ease of verification. It provides a logical starting point in patrimonial analysis and may serve as a minimum reference value in certain contexts. Nevertheless, in a going-concern framework centered on future profitability, this method is generally insufficient to reflect the overall economic value of a business.

Approach Based on the Adjusted Net Asset Value (Adjusted NAV)

Adjusted Net Asset Value represents a natural evolution of Net Asset Value. While NAV reflects a strictly balance-sheet value based on historical accounting conventions, Adjusted NAV seeks to align this value with economic reality. It consists of adjusting assets and liabilities to reflect their market value or current economic value. Adjusted NAV therefore follows a dynamic patrimonial logic by eliminating accounting distortions through targeted corrections.

The method begins with NAV and then proceeds to a line-by-line reassessment of assets and, where relevant, liabilities. Tangible fixed assets may be adjusted to their market value where this differs from their net book value. Financial assets are updated to their actual value. Certain provisions may be revised if they appear excessive or insufficient. In addition, identifiable intangible assets not recorded on the balance sheet may be recognized where their value can be reliably measured. Formally, Adjusted NAV may be expressed as follows:

Adjusted NAV = NAV + Unrealized gains – Unrealized losses ± Deferred taxes on adjustments

Let us consider a simplified example in Swiss francs. A company reports a Net Asset Value (NAV) of CHF 1,500,000. An appraisal determines that real estate recorded at CHF 2,000,000 has a market value of CHF 2,400,000, resulting in an unrealized gain of CHF 400,000. Assuming an effective tax rate of 15 percent, the deferred tax on this unrealized gain amounts to CHF 60,000 (400,000 × 15 percent). Adjusted NAV is therefore calculated as follows:

CHF 1,500,000 + CHF 400,000 – CHF 60,000 = CHF 1,840,000

If, at the same time, inventory is overstated by CHF 100,000, this unrealized loss reduces the value directly, without generating additional tax if it is already deductible. Adjusted NAV would then be revised to:

CHF 1,840,000 – CHF 100,000 = CHF 1,740,000

This method offers a clear strength: it provides an economically coherent patrimonial estimate by taking into account latent gains and the associated deferred taxation. It is particularly relevant for real estate companies, holding structures or businesses whose assets are recorded at historical values that no longer reflect market conditions.

Nevertheless, Adjusted NAV remains a static approach. It does not capture future earning capacity or growth prospects. It primarily serves as a patrimonial reference point that frames a valuation but is rarely sufficient on its own in a dynamic going-concern context.

Approach Based on Substantial Value

Under Swiss law and practice, substantial value most commonly refers to the net book value of shareholders’ equity as reported in the balance sheet. It therefore corresponds to the equivalent of Net Asset Value, that is, the difference between total assets and total liabilities. Substantial value is based on a strictly patrimonial and balance-sheet approach, without projecting future cash flows or explicitly incorporating profitability dynamics.

The method is straightforward: substantial value is equal to book shareholders’ equity as derived from financial statements prepared in accordance with applicable standards, notably the Swiss Code of Obligations or Swiss GAAP FER.

Formally:

Substantial Value = Total assets – Total liabilities = Book shareholders’ equity

Consider an example in Swiss francs. A company reports total assets of CHF 8,000,000 and total liabilities of CHF 5,500,000. Shareholders’ equity therefore amounts to CHF 2,500,000. The substantial value of the company is CHF 2,500,000, absent exceptional adjustments decided within a specific framework.

In certain Swiss practices, particularly for tax purposes or under the so-called practitioners’ method, substantial value may be combined with an earnings value to determine a weighted average valuation. However, taken in isolation, it remains a purely accounting-based measure reflecting the net assets recorded on the balance sheet.

The strength of substantial value lies in its simplicity, transparency, and traceability. It is easily verifiable, objectively determinable, and legally stable. It often serves as a minimum reference value in patrimonial or tax contexts, or in situations where the continuity of operations is uncertain.

Its limitations are similar to those of Net Asset Value. It does not incorporate unrealized gains not recorded in the accounts, unrecognized intangible assets, or future earning capacity. In a profitable and growing company, substantial value is frequently lower than the overall economic value. It represents a patrimonial snapshot at a given point in time rather than a dynamic estimate of value creation.

Strengths of the Cost Approach in a Corporate Valuation Context

In a corporate valuation context, the cost approach presents a major strength in that it establishes an objectively verifiable patrimonial floor based on auditable data. NAV, Adjusted NAV and substantial value provide a rational anchor that is independent of forward-looking assumptions which may be uncertain. Within a valuation mandate, this method allows the valuator to secure a coherent minimum base before integrating dynamic approaches.

It is particularly relevant where the value of the business rests significantly on identifiable assets such as real estate, shareholdings or industrial equipment, or where the mandate is conducted under a prudent framework, notably for tax or succession purposes. In such cases, the cost approach contributes to framing the valuation range and avoiding excessive overvaluation linked to optimistic projections.

Adjusted NAV further strengthens this robustness by incorporating unrealized gains and the related deferred taxation. In a corporate valuation context, this correction aligns book value with economic reality while accounting for the theoretical tax consequences of adjustments. The patrimonial approach thus becomes an instrument of consistency control vis-à-vis methods based on future cash flows.

Finally, within a comprehensive valuation framework, the cost approach plays a comparative reference role. It enables the valuator to assess whether prospective methods produce results consistent with the company’s patrimonial substance. In doing so, it enhances the overall methodological robustness of the valuation process.

Limitations and Weaknesses of the Cost Approach in a Corporate Valuation Context

In a going-concern valuation context, the principal limitation of the cost approach lies in its static nature. It measures wealth at a specific point in time without integrating the company’s future capacity to generate value. Yet in most valuation mandates, value primarily depends on anticipated profitability and the risk profile of future cash flows.

As a result, the method may lead to significant undervaluation of businesses that are high-performing, innovative or heavily oriented toward services and intangible assets. Human capital, technology, customer relationships and strategic positioning are not fully reflected through a purely patrimonial analysis. In a modern economy, this limitation is structural.

Moreover, although Adjusted NAV is economically more relevant than NAV, it remains dependent on assumptions regarding market values and deferred taxes. These estimates may introduce elements of judgment and require rigorous justification within the valuation report. The method is therefore sensitive to the quality of the underlying appraisals.

In a transactional framework, the cost approach does not incorporate acquirer-specific synergies or strategic effects associated with a change of control. It reflects an autonomous patrimonial value rather than a strategic value. Consequently, when used in isolation in the valuation of an operating business, it often results in an incomplete estimate and must be complemented by income-based or market-based approaches.

Market Approach: Comparables, Direct and Indirect Trading Multiples, and Transaction Multiples

The market approach consists of estimating a company’s value by reference to observed prices for comparable companies or for transactions in the same sector. It rests on the idea that the market—through investment decisions by financial or industrial actors—aggregates collective information regarding growth expectations, risk level, and sector outlook.

However, this approach can only be implemented meaningfully if a rigorously selected comparable set or reference universe is first constructed. Determining that comparable universe requires fine analysis of the sector, competitive positioning, size, growth profile, profitability, and risk level. This methodological step is decisive, because valuation quality depends directly on the coherence and homogeneity of the selected panel.

This requirement applies equally to direct trading multiples, indirect trading multiples, and transaction multiples.

In a business evaluation context, especially for transactional purposes, the market approach anchors the analysis in observable data, provided that the chosen reference universe is economically relevant and methodologically defensible.

Direct Trading Multiples Method

Direct trading multiples provide a direct estimate of equity value because they relate market capitalization to a financial metric available to shareholders. They therefore reflect post-debt valuation, implicitly incorporating capital structure. The main direct multiples used in business valuation are P/E, Price-to-Book, Price/Cash Flow, and the PEG ratio.

Price/Earnings Ratio (P/E) is the most widely used. It is the ratio of market capitalization to net income:

P/E = Market capitalization / Net income

P/E measures how much investors are willing to pay for one unit of net profit. The implicit metric is after-tax net income, therefore after creditors have been paid. It already incorporates leverage effects. Thus, two companies with identical EBITDA but different debt levels may display different P/Es. P/E is particularly relevant when net profitability is stable and representative of sustainable economic performance.

Price/Book (P/B) relates market capitalization to book equity:

P/B = Market capitalization / Book equity

It measures the market value attributed to each unit of equity recorded on the balance sheet. It is often used in banking or financial sectors, where the balance sheet is a central performance indicator. The implicit metric is book equity, assuming it reasonably reflects economic substance.

Price/Cash Flow (P/CF) relates market capitalization to cash flows generated for shareholders:

P/CF = Market capitalization / Net cash flow

The implicit metric can vary by practice: after-tax operating cash flow, free cash flow to equity, or cash flow from operations. This multiple has the advantage of reducing the impact of depreciation policies and accounting conventions by focusing on actual cash generation.

PEG ratio (Price/Earnings to Growth) complements P/E by integrating expected earnings growth:

PEG = P/E / Expected net income growth rate

It helps assess whether a high P/E is justified by strong future growth. The implicit metric thus combines net income and its expected growth rate. This ratio is particularly used in fast-growing sectors where valuation depends heavily on development prospects.

In a business evaluation context, the direct trading multiples method has the strength of directly targeting equity value, making it especially relevant when the engagement focuses on valuing shares or units. It reflects market perceptions of earnings or equity and implicitly incorporates cost of capital and growth expectations.

However, this method has structural limitations. The metrics used—net income, cash flow, or book equity—are influenced by capital structure, leverage policy, and accounting conventions. Two economically comparable companies financed differently can show materially different multiples. In addition, listed companies benefit from liquidity, transparency, and market depth that exceed those of private companies. In most cases, applying trading multiples to a private company therefore requires an illiquidity discount to reflect the absence of an organized market for the valued securities. This issue of premia and discounts—especially illiquidity discounts and control premia—is a central methodological topic and warrants dedicated treatment. Finally, the dependence of direct multiples on capital structure naturally leads many professional engagements to prefer indirect trading multiples based on enterprise value, which allow a more rigorous neutralization of leverage effects.

Indirect Trading Multiples Method

Indirect trading multiples first estimate enterprise value using observed data for comparable listed companies. Equity value for the company being valued is then derived by deducting net debt. They are termed “indirect” because they first estimate the overall value of operating activity before financial adjustment. Their main interest lies in neutralizing leverage effects, enabling homogeneous comparisons among companies with different debt structures. By using listed companies, this approach benefits from transparency and data availability, but it requires rigorous comparability analysis and appropriate adjustments when applied to a private company.

EV/Revenue is the most aggregated multiple:

EV/Revenue = Enterprise Value / Revenue

The implicit metric is gross activity volume, regardless of profitability. This multiple is mainly used when profitability is unstable, low, or still being built—especially in technology, innovative, or high-growth sectors. It reflects market expectations regarding the potential to convert revenue into future margins. However, it does not account for cost structure and can mask significant profitability differences among comparables.

EV/EBITDA is an intermediate multiple:

EV/EBITDA = Enterprise Value / EBITDA

The implicit metric is operating performance before depreciation, interest, and taxes. It reflects the gross capacity to generate operating cash flow. It is widely used because it reduces the impact of depreciation policies and enables fairly homogeneous comparisons. It is particularly relevant in sectors where asset bases and depreciation structures differ materially.

EV/EBIT is a more conservative approach:

EV/EBIT = Enterprise Value / Operating income (EBIT)

EBIT includes depreciation and therefore reflects economic consumption of assets. This multiple is particularly suited to capital-intensive industries where asset renewal is critical. It offers a view closer to true economic operating profit and better incorporates investment structure.

The key advantage of indirect multiples lies in their ability to compare companies on an operational basis neutral with respect to financing. They are therefore frequently preferred in professional business valuation engagements, particularly in M&A contexts. However, their relevance depends closely on the quality of the comparable panel and normalization of the financial metrics used.

Transaction Multiples Method

The transaction multiples method estimates company value by reference to completed disposals of comparable companies. Unlike trading multiples, which rely on listed firms, this method relies on prices paid in real equity transfers. It therefore reflects concrete investment decisions and the negotiation conditions specific to each deal.

As with any market approach, building a comparable sample is essential. Selected transactions must be consistent with the target company in terms of sector, geography, and economics. The size of the target, its profitability profile, its growth dynamics, and the macroeconomic context at the time of the transaction must be rigorously analyzed.

Transaction multiples are generally expressed as EV/Revenue, EV/EBITDA, or EV/EBIT to neutralize capital structure. Observed enterprise value in the transaction is compared to a normalized operating metric of the target at the time of the transaction. Equity value is then obtained by deducting net debt.

A key methodological element is the degree of control transferred. A majority acquisition conferring control generally includes a control premium reflecting the ability to direct strategy, appoint governance bodies, and decide distribution policy. Conversely, a minority transaction may reflect a minority discount due to lack of decision-making power. These premia or discounts directly affect the observed multiple.

In practice, when comparable deals involve majority acquisitions, observed multiples may incorporate an implicit premium. If the valuation concerns a minority stake (or vice versa), neutralizing this effect may be necessary to ensure comparability. This is generally done through a percentage adjustment based on market practice and empirical studies on control premia. Without adjustment, the chosen multiple could overstate or understate the value of the stake being valued.

Finally, transaction multiples may incorporate buyer-specific elements, notably strategic or industrial synergies. These synergies are not necessarily transferable to any investor. The evaluator must therefore distinguish the target’s standalone intrinsic value from the strategic value specific to a given acquirer.

Thus, the transaction multiples approach is particularly relevant in an M&A context, provided that the nature of control transferred is precisely analyzed and, where appropriate, observed multiples are adjusted to ensure methodological consistency.

Strengths of the Market Approach in a Business Evaluation Context

In a business evaluation context, the market approach has a key methodological strength: it allows estimated value to be confronted with observable economic references. Whether based on trading multiples from comparable listed firms or transaction multiples from completed deals, the approach relies on prices actually observed in the real economic environment. It is therefore an empirically grounded anchor, especially relevant when valuing a company for sale, acquisition, or capital restructuring.

It also positions the valued company within its competitive ecosystem. Comparing it with a structured panel of comparable companies—selected using rigorous sector, geographic, and financial criteria—provides a relative reading of performance and risk profile. In a business evaluation engagement, this comparative dimension helps frame the value range and test the coherence of intrinsic methods.

In transactional contexts, observed multiples reflect levels accepted by strategic or financial investors. They implicitly incorporate market conditions, sector risk perceptions, and growth expectations. The market approach thus becomes an arbitration tool between theoretical value and negotiable value.

Finally, it plays a fundamental role in cross-validation. When value derived from cash flow discounting or patrimonial approaches converges with market levels, the robustness of the evaluation is strengthened.

Limitations and Weaknesses of the Market Approach in a Business Evaluation Context

In a business evaluation context, the market approach remains dependent on the quality of the chosen reference universe. The absence of perfectly homogeneous comparables can generate significant distortions. Differences in size, capital structure, governance, or growth dynamics can affect the relevance of applied multiples.

It is also sensitive to economic cycles. Trading multiples may reflect phases of financial exuberance or contraction independent of the valued company’s fundamentals. Mechanical application without critical analysis may thus lead to excessive or insufficient estimates.

Moreover, using trading multiples to value a private company generally requires applying an illiquidity discount. Likewise, transaction multiples may incorporate control premia or acquirer-specific synergies. If the valuation concerns a minority stake or a standalone value, methodological neutralization may be required to preserve analytical consistency.

Finally, the market approach alone does not identify intrinsic value drivers. It reflects an external observation of price without analyzing future cash flows, strategy, or internal capabilities. In a business evaluation engagement, it must therefore be integrated into a broader approach combining patrimonial and income methods to achieve a structured, reasoned, and economically coherent estimate.

Income Approach: Earnings Value and Discounted Cash Flow (DCF) Method

In a business evaluation context, the income approach rests on a fundamental principle of finance: the value of a company corresponds to the discounted sum of the economic flows it can generate, given the risk associated with those flows. It is not limited to mechanically projecting future results; it also integrates investors’ return requirements, grounded both in observed historical performance and in reasonable expectations of future profitability. Value is thus determined by the balance between sustainable earning capacity and perceived risk level. Unlike the patrimonial approach, centered on a stock of assets at a given time, or the market approach, based on external comparative references, the income approach focuses on the company’s internal economic fundamentals and its own value-creation dynamics.

Earnings Method Based on EBITDA

In a business evaluation context, the earnings method based on EBITDA consists of determining enterprise value from a normalized EBITDA representative of recent performance, capitalized by the weighted average cost of capital (WACC). This approach relies on a stabilization logic: it assumes that past performance, when representative and sustainable, provides a relevant basis to estimate future earning capacity.

Concretely, the method calculates the average EBITDA of the last three fiscal years, provided they are representative and adjusted for non-recurring items. The average smooths cyclical effects and extracts a normalized economic performance. The chosen EBITDA should exclude exceptional income and expenses, one-off effects, and any distortion that could alter the true economic reading.

The formula can be expressed as:

Enterprise Value = Average EBITDA of the last three years / WACC

WACC reflects the return required by all capital providers, weighted by a target capital structure. It integrates the cost of equity and the after-tax cost of debt. Using WACC is coherent insofar as EBITDA is a pre-financing metric (before remuneration of creditors and shareholders).

This method implicitly assumes that observed performance is sustainable over time and that future growth is low or embedded in the capitalization rate. It is particularly suited to mature businesses with relatively stable margins and investment structures.

However, this approach has limitations. EBITDA does not account for investments required to maintain operations nor changes in working capital needs. It can therefore overstate value if the business requires significant capital expenditures. Moreover, using a historical average assumes the last three years reflect a normal, non-transitory situation.

In a business evaluation engagement, the EBITDA earnings method is thus a simplified and pragmatic approach, relevant when economic stability is established, but one that should be cross-checked against a more dynamic analysis, notably through discounted cash flows.

Earnings Method Based on Net Income

In Swiss business valuation practice, the earnings method based on net income has a notable specificity. It is embedded in Swiss tax practice and relies on capitalizing an average net income by a capitalization rate set by the Swiss Tax Conference (SSTC/CSI). This approach is used notably for tax valuations, estates, or business transfers.

Methodologically, a representative average net income is determined, generally based on the last three fiscal years, subject to adjustments removing extraordinary or non-recurring items. The goal is to identify sustainable earning capacity reflecting normal economic performance.

The formula can be expressed as:

Equity Value = Average net income of the last three years / CSI capitalization rate

Unlike approaches using a company-specific cost of equity (e.g., via CAPM), the capitalization rate here is normative and published by the tax authorities. By way of illustration, this rate was 8.75% in 2024. It reflects a theoretical required return for a standardized business risk profile, without fine sector differentiation.

Using a uniform rate ensures comparability and legal certainty for tax purposes. It enables simplified and consistent application across taxpayers. However, this standardization is also a limitation: the rate does not necessarily reflect the company’s specific risk profile or sector economic conditions.

Outside a strictly tax framework, this method may be less suitable than individualized approaches incorporating a discount rate derived from the company’s characteristics. Nevertheless, it remains a reference tool in Swiss practice, notably when combined with substantial value in the practitioners’ method.

Discounted Cash Flow (DCF) Method

In a going-concern business evaluation context, the Discounted Cash Flow (DCF) method is the most advanced analytical tool within the income approach. It is based on the fundamental principle that a company’s value corresponds to the discounted sum of future cash flows it can generate, adjusted for the risk associated with those flows. DCF does not merely capitalize a historical result; it explicitly models the company’s future economic dynamics.

When an approach based on free cash flow available to all capital providers (Free Cash Flow to Firm, FCFF) is used, enterprise value is expressed as follows:

where FCFt is the free cash flow for year t, WACC is the weighted average cost of capital, n is the explicit forecast horizon, and TV is the terminal value.

Free Cash Flow to Firm is generally determined as follows:

This cash flow corresponds to operating profit after tax, plus non-cash charges, minus net investments and changes in working capital. It reflects the company’s real ability to generate liquidity independently of its capital structure.

Terminal value represents economic value beyond the explicit forecast horizon. In practice, it is frequently determined using the perpetual growth model:

where g is the sustainable long-term growth rate. This parameter must be consistent with macroeconomic and sector prospects. A modest change in g can significantly impact derived value, requiring rigorous sensitivity analysis.

Once enterprise value is determined, equity value is obtained by deducting net debt:

(formula presentation)

Methodological consistency is central. When cash flows are FCFF, the appropriate discount rate is WACC. Conversely, if flows available to shareholders (Free Cash Flow to Equity) are used, discounting must be done at the cost of equity.

In a business evaluation engagement, DCF has the major advantage of explicitly incorporating the fundamental drivers of value creation: growth, profitability, investment structure, and risk profile. It also enables sensitivity analyses to frame a value range. However, its robustness depends directly on the quality of assumptions and a deep understanding of the valued company’s business model.

Strengths of the Income Approach in a Business Evaluation Context

In a business evaluation context, the income approach has a key conceptual strength: it rests on the valued company’s intrinsic economic fundamentals. Unlike patrimonial or market approaches, it depends neither on a balance-sheet snapshot nor exclusively on external comparables, but on the company’s real ability to generate future cash flows. It thus measures value based on sustainable operating performance and associated risk–return trade-offs.

This approach also offers strong analytical granularity. It explicitly integrates growth assumptions, required investments, cost structure, competitive dynamics, and sector profile. In a strategic or transactional engagement, it is particularly relevant to assess the coherence of a business plan and model different economic scenarios.

Another advantage lies in its capacity to frame a value range through sensitivity analyses. By varying key parameters such as discount rate, terminal growth, or operating margins, the evaluator can measure value elasticity to assumptions. This enhances methodological transparency and supports structured dialogue with management, investors, or tax authorities.

Finally, the income approach is particularly suited to companies whose value primarily depends on future earning capacity—especially service, technology, or innovative businesses—where patrimonial substance is secondary to value-creation dynamics.

Limitations and Weaknesses of the Income Approach in a Business Evaluation Context

Despite its theoretical robustness, the income approach has significant limitations. First, it is sensitive to assumptions. Financial forecasts, growth rates, and discount rates necessarily rely on estimates. A modest change in these parameters can result in substantial differences in derived value.

It also requires a high level of data quality and reliability. For businesses with highly volatile results, limited history, or unstable economic environments, the ability to credibly project cash flows may be reduced. Forecast uncertainty is therefore a structural limitation.

In addition, determining discount rates can introduce subjectivity. Computing the cost of equity, estimating beta, market risk premium, or cost of debt requires methodological choices that influence valuation outcomes. This dimension requires rigorous justification in the valuation report.

Thus, the income approach may be less relevant where going concern is uncertain or where value depends mainly on identifiable tangible assets. It must then be confronted with patrimonial and market approaches to ensure a balanced and economically coherent evaluation.

Real Options Approach: Black–Scholes–Merton (BSM) and Cox–Ross–Rubinstein (CRR)

In a business evaluation context, the real options approach aims to explicitly integrate managerial flexibility into value determination. Unlike traditional methods such as DCF, which often assume a fixed and passive operating plan, the real options approach recognizes that management has strategic levers: delaying an investment, abandoning it, expanding it, reducing it, or changing its scope.

This approach is grounded in the theory of financial option valuation. The work of Black, Scholes, and Merton (1973) formalized the valuation of options on financial assets, while the binomial model of Cox, Ross, and Rubinstein (1979) offered a discrete, more intuitive approach. These tools were gradually transposed to the valuation of investment projects and, by extension, to business evaluation when it includes significant strategic options.

Real Options Method Derived from Black–Scholes–Merton (BSM)

The Black–Scholes–Merton model is a continuous approach based on the stochastic dynamics of underlying assets. Applied to business evaluation, it involves assimilating a project or strategic opportunity to a financial option. For example, a future investment can be interpreted as a call option: the company has the right, but not the obligation, to invest capital to generate a future cash flow.

The general BSM formula for a call option is:

where:

- S0 is the current value of the underlying asset (e.g., the present value of expected project cash flows),

- K is the investment cost (strike price),

- r or Rf is the risk-free rate,

- T is time to maturity,

- N(d1) and N(d2) are cumulative normal distribution functions,

- σ is the volatility of the underlying asset.

In a business evaluation context, volatility reflects uncertainty around future project cash flows. The higher uncertainty is, the higher the strategic option value becomes. This feature fundamentally differentiates real options from traditional DCF: uncertainty is not only a risk factor reducing value through a higher discount rate, but also a potential source of opportunity.

However, applying BSM relies on strong assumptions, notably log-normality of returns and the existence of a complete market allowing replication. These assumptions may limit the precision of a direct transposition to real-world industrial projects.

Real Options Method Derived from Cox–Ross–Rubinstein (CRR) | Binomial Tree

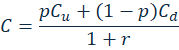

The Cox–Ross–Rubinstein model is a discrete binomial approach. Unlike BSM, it models the evolution of the underlying asset value over successive periods, during which value can move up or down based on predetermined factors.

Option value is determined by discounting future option payoffs weighted by so-called risk-neutral probabilities. The basic one-period binomial formula can be written:

where:

- Cu and Cd are option values in up and down states,

- P is the risk-neutral probability,

- r or Rf is the risk-free rate.

The key advantage of CRR is flexibility. It allows easier integration of sequential decisions such as staged expansion, early abandonment, or investment deferral. It is particularly suited to industrial or technological projects involving multiple decision steps.

In a business evaluation context, this method is relevant when value depends on uncertain assets—for example patents, R&D projects, or natural reserves—and when strategic flexibility is a key driver of value creation.

The real options approach does not replace traditional business evaluation methods; it complements them when uncertainty and strategic flexibility play a determining role. It enriches the analysis by capturing a dimension that deterministic models tend to underestimate.

Strengths of the Real Options Approach in a Business Evaluation Context

In a business evaluation context, the real options approach has a key conceptual strength: it explicitly integrates strategic flexibility into value determination. Unlike deterministic models such as DCF, which assume a fixed operating plan, real options recognize that management has dynamic decision-making power. The ability to defer an investment, abandon a project, expand an activity, or adapt strategy is itself a source of value.

This approach is particularly relevant for businesses operating in uncertain or technological environments. In sectors related to R&D, patents, biotechnology, natural resources, or infrastructure projects, a significant part of value lies in future opportunities rather than stabilized current cash flows. The real options approach can then capture a value component that traditional methods tend to undervalue.

It also provides a better understanding of the uncertainty–opportunity trade-off. While uncertainty is typically treated in traditional models as a factor reducing value via a higher discount rate, real options models recognize that volatility can increase the value of a strategic option. This is a major theoretical contribution to the analysis of projects with asymmetric upside.

Integrating real options can enrich the analysis by distinguishing the present value of stabilized cash flows from the incremental value linked to growth opportunities. It thus offers a more complete and nuanced view of value creation.

Methodological Limitations and Constraints of the Real Options Approach in a Business Evaluation Context

Despite its theoretical appeal, the real options approach faces significant methodological constraints. First, it is difficult to estimate key parameters, notably the volatility of the underlying asset. Unlike listed financial options, industrial or strategic projects do not have observable price series enabling direct volatility estimation.

Model assumptions, particularly in BSM, rely on idealized conditions such as complete markets and perfect replicability. These assumptions are rarely satisfied in real projects, limiting model precision.

Moreover, identifying the strategic option itself requires deep professional judgment. Not all managerial flexibilities are easily modelable. The increasing complexity of decision trees in binomial models can also make analysis difficult to communicate to non-specialist third parties.

Real options should not substitute for fundamental methods such as DCF. They are a complement intended to enrich analysis when specific and measurable opportunities exist. Used in isolation, they could lead to overvaluation if assumptions are not tightly framed.

The Practitioners’ Method: Swiss Tax Method for Valuing Unlisted Shares

In Swiss business evaluation practice, the practitioners’ method is a structured reference, notably for tax purposes. It derives from recommendations by the Swiss Tax Conference (CSI) on the valuation of unlisted securities and aims to determine a harmonized tax value for wealth tax or certain transfers.

This method is based on a combined logic, articulating two components:

- an earnings value, based on capitalizing average net income,

- a substantial value, corresponding to book equity (or possibly adjusted).

The objective is to produce a balanced value reflecting both earning capacity and patrimonial substance.

Earnings value is determined by calculating the average net income of the last three fiscal years (adjusted if necessary), then dividing by the CSI capitalization rate. This rate is normative and identical for all businesses, regardless of specific risk profile.

The formula can be expressed as:

By way of illustration, the capitalization rate was 8.75% in 2024.

Substantial value corresponds to book equity:

Substantial value = Assets − Liabilities

Tax value of the shares is then determined using a standard weighting:

Earnings value is weighted at two-thirds, while substantial value accounts for one-third.

This weighting reflects the primacy of earning capacity in a going-concern logic while retaining a patrimonial anchor.

The practitioners’ method is mainly used in Swiss tax contexts, especially for valuing unlisted shareholdings held by individuals. It aims to ensure intercantonal uniformity and legal certainty.

It is not intended to reflect market value in a transactional context. The normative capitalization rate does not account for company-specific risk, sector, or macroeconomic conditions.

The practitioners’ method sits between patrimonial and income approaches. It is a hybrid, simplified, and standardized method suited to the Swiss tax framework but can differ materially from an economic valuation performed in an M&A context.

Sensitivity Analysis and Determination of a Value Range

In a business evaluation context, determining value cannot reasonably be limited to a single fixed amount. Every estimate rests on assumptions—growth, margins, discount rate, capital structure, selected comparables—that inherently contain uncertainty. Sensitivity analysis is therefore an essential methodological step. It measures the impact of changes in key parameters on derived value and frames analysis within an economically coherent value range.

In a DCF, sensitivity primarily concerns discount rate (WACC), perpetual growth rate, and key operating assumptions. A limited change in WACC or terminal growth can produce significant valuation differences. Similarly, changes in normalized margins, investment pace, or working capital variations can materially shift value. Sensitivity analysis identifies dominant variables and tests model robustness.

In the market approach, sensitivity arises from other key parameters. Choosing the average versus the median multiple can significantly influence results. Median is often preferred to limit outlier impact, whereas average may be relevant when the sample is homogeneous. This methodological choice must be explicitly justified because it can alter the final estimate.

Direct trading multiples (P/E, P/B, P/CF), indirect trading multiples (EV/Revenue, EV/EBITDA, EV/EBIT), and transaction multiples are also sensitive to the application of premia or discounts. An illiquidity discount may be required when applying trading multiples to a private company. A control premium may be incorporated or neutralized depending on whether the valued stake is majority or minority. Certain deals include acquirer-specific synergies that may require adjustment to reflect standalone value. These percentage adjustments directly affect final value.

Thus, sensitivity in the market approach is not limited to mechanical variation of the multiple; it also includes analysis of comparable selection, control level transferred, and liquidity adjustments. Combining these parameters can materially shift the estimated value.

The objective is not to produce arbitrary dispersion, but to determine a justified value range resulting from method convergence and controlled variation of key assumptions. This range is a rational arbitration tool in transactional, tax, or strategic contexts.

Determining a value range strengthens analytical credibility. It explicitly recognizes the uncertainty inherent to economic estimation while structuring it through a methodical and reasoned approach. The selected summary value then sits within this range based on professional judgment consistent with the overall work performed.

Summary Table of Valuation Approaches and Methods in Business Evaluation

The relevance of a method depends on the engagement framework, the company’s economic profile, and the pursued objective (transactional, tax, strategic, litigation, or patrimonial). No approach should be applied automatically. The robustness of an evaluation rests on methodological coherence and the reasoned confrontation of several approaches.

The table below summarizes the main methods developed in this article and their preferred contexts of application.

Other Valuation Approaches and Methods in Business Evaluation

In a business evaluation context, certain situations require the use of complementary or alternative methods beyond patrimonial, market, income, or real options approaches. These methods, sometimes more specific or sector-based, respond to particular economic logics. They are not universal standards, but may be relevant depending on the nature of the activity, the company’s life cycle, or the purpose of the engagement.

A first category includes so-called empirical or sector methods. Some industries have historically developed their own valuation rules based on specific operating indicators: multiples of subscriber counts in telecommunications, value per hotel bed, per square meter in commercial real estate, or per assets under management in asset management. These approaches rely on market conventions observed in comparable deals. They can provide a quick reference point, but must be used cautiously and systematically cross-checked against more fundamental methods.

A second category involves liquidation value methods. In certain situations—especially when going concern is uncertain or the firm holds easily saleable assets—the evaluator may determine value by simulating an orderly disposal of assets, net of liabilities and liquidation costs. This differs from substantial value in that it incorporates assumptions about actual realization of assets at potentially discounted market prices.

A third approach is the Sum of the Parts (SOTP) method. It is particularly relevant for diversified groups operating across distinct business segments. Each division is valued separately using the most appropriate method for its profile (DCF, multiples, patrimonial value), and the values are aggregated. This can reveal gaps between consolidated value and the sum of components, especially when divisions have very different growth and risk profiles.

One can also mention methods based on economic value creation, such as Economic Value Added (EVA). This approach measures performance by comparing after-tax operating profit to the cost of invested capital. Although primarily used as a strategic steering tool, it can be integrated into an evaluation framework consistent with discounted cash flow modeling.

Finally, in specific contexts—especially early-stage start-ups—private equity-style methods may be used. The venture capital method, for example, determines a target future value and then discounts it back to present value using a high required return rate reflecting significant project risk. This approach is widely used during seed or growth fundraising rounds.