Financial Due Diligence: Definition, Methodology, Steps and Approaches

Financial Due Diligence | Acquisition audit, VDD, QoE, red flags and M&A case study

Introduction: Financial Due Diligence — The Truth Test of a Transaction

In any merger or acquisition transaction, the price negotiated between buyer and seller rests on assumptions — assumptions about the quality of earnings, the soundness of the balance sheet, the reality of cash flows, and the sustainability of the business model. Financial due diligence is the process that allows these assumptions to be verified, hidden risks to be identified, and the parties to be provided with the objective basis necessary for an informed investment decision.

Financial due diligence — also known as an acquisition audit or transactional financial review — is a mission of critical analysis of the financial position of a target company, conducted in the context of a transaction. It does not certify the accounts: it analyses them critically through the lens of the transaction, answering a fundamental question: "Does what the seller presents as the financial reality of its business correspond to what the buyer will actually acquire?"

Too often perceived as an administrative formality, financial due diligence is in reality one of the most powerful tools in M&A practice. It can confirm or challenge an acquisition price, uncover unrecorded liabilities, expose accounting manipulation, or conversely reassure the buyer of the quality of the target. In some cases, it constitutes the only safeguard between a value-creating acquisition and a value-destroying one.

The ICAEW — Institute of Chartered Accountants in England and Wales — defines financial due diligence as a process whose primary objective is to improve knowledge of a company's financial performance, to identify red flags and risks so that buyers and financers can make an informed decision. (ICAEW Corporate Finance Faculty, Financial Due Diligence Guideline, PwC, 2024.) This framework, which now carries authority in European M&A practice, explicitly distinguishes buy-side due diligence and the Vendor Due Diligence (VDD) — a distinction this article addresses in detail.

In mid-market M&A transactions in France and Switzerland, financial due diligence is too often conducted superficially — a few days of analysis based on annual accounts, without in-depth investigation into the quality of earnings, without normalised working capital analysis, without systematic identification of off-balance-sheet commitments. The consequences are well known: unadjusted acquisition price, unidentified liabilities, uncalibrated earn-outs, insufficient contractual warranties. Financial due diligence is not a process formality — it is a decision-making tool.

This article presents a complete financial due diligence methodology, structured around five key themes. We will first distinguish the two complementary forms of due diligence — the acquisition audit on the buyer side and the Vendor Due Diligence on the seller side — before examining the organisation of an effective financial data room. We will then detail the QoE (Quality of Earnings) methodology with specific restatements by financial statement — income statement, balance sheet, net debt and working capital — followed by the main red flags and warning signals to monitor. The whole will be illustrated by a concrete case study: the financial due diligence of a SaaS acquisition at €/CHF 30m.

Definition: What Is Financial Due Diligence?

Financial due diligence — also known as an acquisition audit or transactional financial review — is an in-depth analysis of the financial position of a target company, conducted in the context of a transaction (acquisition, disposal, fundraising, LBO). Its objective is to assess the quality and reliability of the financial information provided, and to identify risks and adjustments likely to affect the price or conditions of the transaction.

It differs fundamentally from a statutory audit or external audit, whose objective is to certify the regularity and fairness of the annual accounts. Financial due diligence does not certify the accounts — it analyses them critically through the lens of the transaction, answering the fundamental question:

"Does what the seller presents as the financial reality of its business correspond to what the buyer will actually acquire?"

Would you like to have your business, its assets or financial instruments valued, sell it, or conduct a financial due diligence?

Hectelion handles all these operations in France and Switzerland — business sale, divorce, shareholders agreement, taxation, assets, financial instruments and financial due diligence.

→ Book a call — 30 minutes, confidential

The Different Types of Due Diligence

Financial due diligence forms part of a broader set of complementary due diligence workstreams, generally conducted in parallel within an M&A transaction :

Origins and Framework of Financial Due Diligence

The concept of due diligence originated in the United States in the wake of the Securities Act of 1933. This foundational text does not contain the term "due diligence" itself — it emerged from legal practice as the term designating the "reasonable investigation" that Section 11 of that same text required of financial intermediaries (underwriters) to exonerate their liability in the event of inaccuracy in a prospectus. (FindLaw, Underwriter Due Diligence in Securities Offerings, 2008.) The concept subsequently progressively extended to all M&A transactions as a standard of good professional practice, well beyond its original scope.

In France, financial due diligence is not formally required by law for private transactions, but it constitutes a de facto obligation in the vast majority of M&A transactions involving institutional investors, private equity funds, or bank financing. In Switzerland, the same practices prevail, with particular attention paid to the specificities of Swiss law of obligations (CO) and the market practices specific to the Swiss market.

The professional standards applicable to financial due diligence are defined by several frameworks: the ICAEW (Institute of Chartered Accountants in England and Wales), the ACCA, and the practices of major Transaction Advisory Services firms (Big 4 and Tier 2). In France, the Compagnie Nationale des Commissaires aux Comptes (CNCC) and the Conseil Supérieur de l'Ordre des Experts-Comptables (CSOEC) govern transactional financial review assignments.

Why Conduct Financial Due Diligence?

For the Buyer

For the buyer, financial due diligence fulfils three essential functions. It first allows verification that the acquisition price is justified by the actual financial performance of the target — and to identify the restatements that might lead to a price revision. It then allows hidden risks to be identified — unrecorded liabilities, litigation, off-balance-sheet commitments, critical dependencies — that could affect the value of the business post-acquisition. Finally, it provides the factual elements necessary for negotiating the asset and liability warranty (GAP) clauses, earn-outs, and price adjustment mechanisms.

For the Seller

For the seller, due diligence — particularly in its Vendor Due Diligence (VDD) form — allows the transaction process to be accelerated by providing buyers with homogeneous, verified, and defensible financial information. It reduces buyers' supplementary information requests, minimises disruption to management and finance teams, and reinforces the credibility of the sale file. It can also allow early identification of issues that might give rise to discussions or discounts, in order to address them proactively before opening the process.

For Private Equity Funds and Banks

In the context of an LBO or fundraising transaction, financial due diligence is a sine qua non condition of financing. Lending banks and equity investors systematically require an independent financial due diligence report to validate their modelling assumptions and satisfy the requirements of their investment committees. It also constitutes a reference tool for negotiating financial covenants and protection clauses.

The Two Types of Financial Due Diligence: Acquisition Audit and VDD

A: The Acquisition Audit (Buy-Side Due Diligence)

The acquisition audit is the most classic form of financial due diligence. It is commissioned by the buyer or investing fund, generally after signature of a letter of intent (LOI) or memorandum of understanding (MOU). It is conducted by an independent firm mandated by the buyer, which accesses the target's financial information via a data room.

Its specific objectives are to identify normalised EBITDA adjustments (Quality of Earnings), to validate the level of net financial debt and normalised working capital retained in the valuation, to detect unrecorded or under-provisioned liabilities, and to provide the factual elements necessary for negotiating the SPA (Share Purchase Agreement) and associated warranties.

The acquisition audit is by nature confidential and conducted under time pressure — generally between 4 and 8 weeks in a competitive process, sometimes less in bilateral transactions.

B: The Vendor Due Diligence (VDD)

The Vendor Due Diligence is a financial due diligence commissioned by the seller itself, conducted by an independent firm, and made available to potential buyers in the context of a disposal process. Unlike the acquisition audit, the VDD is initiated before the opening of the sale process — sometimes several months in advance — in order to prepare the business for the transaction.

The VDD is increasingly used in continental Europe, particularly in multi-buyer processes (controlled auctions), where the seller wishes to control the flow of information and standardise the documentary base made available to prospective buyers. It allows the strengths of the business to be highlighted while dealing in a controlled manner with issues likely to raise questions.

Its specific objectives are to provide homogeneous, verified, and defensible financial information to all potential buyers, to identify EBITDA restatements and balance sheet issues upstream, to accelerate the buyer's due diligence phase (which can then be limited to a review of the VDD rather than a full investigation), and to strengthen the credibility of the disposal process vis-à-vis the banks financing the acquisition.

C: Comparative Table: Acquisition Audit vs VDD

The Data Room: Organisation and Content

The data room is the space — physical or, most commonly, virtual — in which the seller makes available to buyers all the documents necessary for their due diligence. It constitutes the central support of any financial due diligence mission and directly conditions the quality and fluidity of the process.

Physical Data Room vs Virtual Data Room

The physical data room — a secure room in which due diligence teams access documents on-site — is today almost entirely abandoned for standard M&A transactions. It survives only for transactions involving particularly sensitive documents (defence files, classified data).

Virtual Data Rooms (VDR) are now the norm. The main platforms used in European M&A practice are Datasite (formerly Merrill DataSite), Intralinks, Drooms, and iDeals. These platforms offer advanced features for access rights management, consultation traceability, Q&A (questions and answers between buyers and seller), and reporting on data room activity.

Standard Structure of a Financial Data Room

Framework and Context of Use

Classic M&A and LBO

Financial due diligence is systematic in any business acquisition involving a professional investor or bank financing. In an LBO context, it is of particular importance as due diligence findings directly feed the LBO model — notably the normalised EBITDA serving as the basis for financial leverage, the net financial debt level, and the target working capital negotiated in the SPA.

Fundraising and Financing

In the context of an equity fundraising transaction (Series A, B, growth equity), financial due diligence is conducted by the incoming investing funds. It is generally less exhaustive than in a classic acquisition, but pays particular attention to revenue quality (recurrence, churn, LTV/CAC), the cash runway, and the coherence of the business plan with valuation assumptions.

France vs Switzerland Specificities

Financial Due Diligence in an LBO

In the context of a financial structuring in LBO (Leveraged Buyout), financial due diligence has specific features compared to a classic industrial acquisition. The private equity fund and its lending banks have particular analytical requirements directly linked to the leverage mechanism structuring the transaction.

EBITDA Cash as the Central Indicator

In an LBO, the reference indicator is not accounting EBITDA but EBITDA Cash — that is, EBITDA after deduction of maintenance capital expenditure (recurring CAPEX) necessary to maintain the business, and before non-recurring items. It is on the basis of this EBITDA Cash that banks calibrate their lending capacity and that the fund builds its return on investment model.

Debt Service Coverage Analysis

LBO due diligence systematically includes an analysis of the acquisition debt service capacity — verification that the operating cash flows generated by the target will be sufficient to service the debt (interest and amortisation) in different scenarios (central, stress, worst case). This analysis is based on the calculation of the DSCR (Debt Service Coverage Ratio) and the Leverage Ratio (Net Debt / EBITDA) projected over the LBO horizon (generally 5 to 7 years).

Financial Covenant Analysis

Lending banks impose financial covenants — thresholds on financial ratios (Leverage, DSCR, Interest Cover Ratio) that the company must respect at each test date, generally semi-annual. Financial due diligence in an LBO includes an analysis of the robustness of these covenants in different performance scenarios, in order to identify situations in which a covenant breach might occur.

Acquisition Debt Structure

LBO due diligence also analyses the envisaged financing structure — split between senior debt (secured), mezzanine debt, PIK (Payment-in-Kind), high yield bonds, and equity — in order to validate that the overall leverage level is supportable by the target's cash flow structure. This analysis directly feeds the financial structuring work of the transaction.

Methodology: The 6 Steps of a Financial Due Diligence Mission

Step 1: Mission Scoping and Organisation

The first step consists of precisely defining the scope of intervention, the priority objectives, and the organisation of the mission. This phase includes signing the engagement letter and confidentiality agreements, defining the list of documents to be requested (request list), organising management sessions (management presentations and Q&A with the target's management), and the work schedule. The quality of scoping directly conditions the efficiency and fluidity of the mission.

Step 2: Quality of Earnings (QoE): Analysis of Earnings Quality

Quality of Earnings (QoE) is the analytical core of any financial due diligence. It aims to determine the normalised and recurring EBITDA level of the target — that is, the EBITDA that will serve as the basis for the valuation multiple. This analysis distinguishes three EBITDA levels:

Step 3: Normalised Working Capital and Cash Analysis

Working capital (WC) is one of the elements most frequently subject to manipulation or misinterpretation in an M&A transaction. Financial due diligence analyses historical working capital over 12 to 24 rolling months, identifies its seasonality, and determines the normalised WC — that is, the WC level that will be used as the reference in the SPA price adjustment mechanism.

The analysis covers the three components of working capital: DSO (Days Sales Outstanding — average client payment delay), DPO (Days Payable Outstanding — average supplier payment delay), and DIO (Days Inventory Outstanding — stock turnover period). Anomalies on any of these components are often indicative of risky management practices or pre-transaction working capital manipulation.

Step 4: Net Financial Debt and Off-Balance-Sheet Commitments Analysis

Restated net financial debt is the second major pillar of M&A valuation, alongside normalised EBITDA. It corresponds to the difference between gross financial debt and available cash, adjusted for debt-like items (unprovisioned social liabilities, earn-outs, probable litigation) and cash-like items (R&D tax credits receivable, overpaid taxes). This analysis is critical as it directly determines the price paid by the buyer in equity value.

Step 5: Business Plan and Financial Projections Analysis

The business plan review aims to assess the credibility and robustness of the financial projections presented by management. It analyses the consistency of revenue growth assumptions with historical performance and market context, the reality of operational margin improvement levers, the level of development CAPEX necessary to achieve the plan's objectives, and projected net cash generation. This analysis directly feeds the DCF valuation model.

Step 6: Due Diligence Report and Conclusions

The financial due diligence report is the final deliverable of the mission. It presents in a structured manner the team's conclusions on the quality of financial information, the restatements retained on EBITDA and net debt, the risks identified and their potential impact on value, and the points to be addressed in warranty clauses in the SPA.

Standard Structure of a Financial Due Diligence Report

A financial due diligence report is a dense document, generally structured in 6 to 8 main sections. Below is the standard table of contents used in professional M&A practice:

Specific Restatements by Financial Statement

The technical core of a financial due diligence mission lies in the restatements applied to each financial statement. The following tables present a complete checklist of restatements to examine for each financial statement, as applied in the practice of Hectelion's missions.

Table 1: Income Statement Restatements (QoE)

Table 2: Balance Sheet Restatements

Table 3: Net Financial Debt Restatements

Table 4: Normalised Working Capital Restatements

Price Adjustments from Due Diligence

The findings of financial due diligence directly feed the price negotiation and contractual mechanisms of the transaction.

Revision of the Base Price

If due diligence reveals a normalised EBITDA below that presented by the seller, the acquisition price is mechanically revised downwards, the valuation multiple remaining unchanged. Similarly, a restated net financial debt higher than initially communicated leads to a reduction in the price paid in equity value.

The Price Adjustment Mechanism (Locked Box vs Completion Accounts)

Two main mechanisms allow the final price to be adjusted based on the financial position at closing. In the Locked Box mechanism, the price is fixed definitively on the basis of accounts at a date prior to closing (the locked box date), with contractual protections against value leakage between that date and closing. In the Completion Accounts mechanism, the price is adjusted after closing based on accounts drawn up at the completion date, depending on the difference between net debt and working capital at closing compared to the target values negotiated in the SPA.

Asset and Liability Warranty (GAP / R&W)

The GAP (or R&W in an Anglo-Saxon context) is the contractual mechanism by which the seller warrants to the buyer that the information communicated during due diligence is accurate and complete, and that no undisclosed liability exists at closing. Risks identified during due diligence but not quantifiable with certainty are generally the subject of specific representations in the GAP, allowing the buyer to be indemnified if these risks materialise after closing.

Earn-Out

The earn-out is a conditional pricing mechanism by which part of the acquisition price is only paid to the seller if certain performance objectives are achieved after closing. It is frequently used when due diligence reveals significant uncertainty over the business plan projections — particularly in acquisitions of start-ups or high-growth companies whose future trajectory is difficult to validate.

Cost and Timing of a Financial Due Diligence Mission

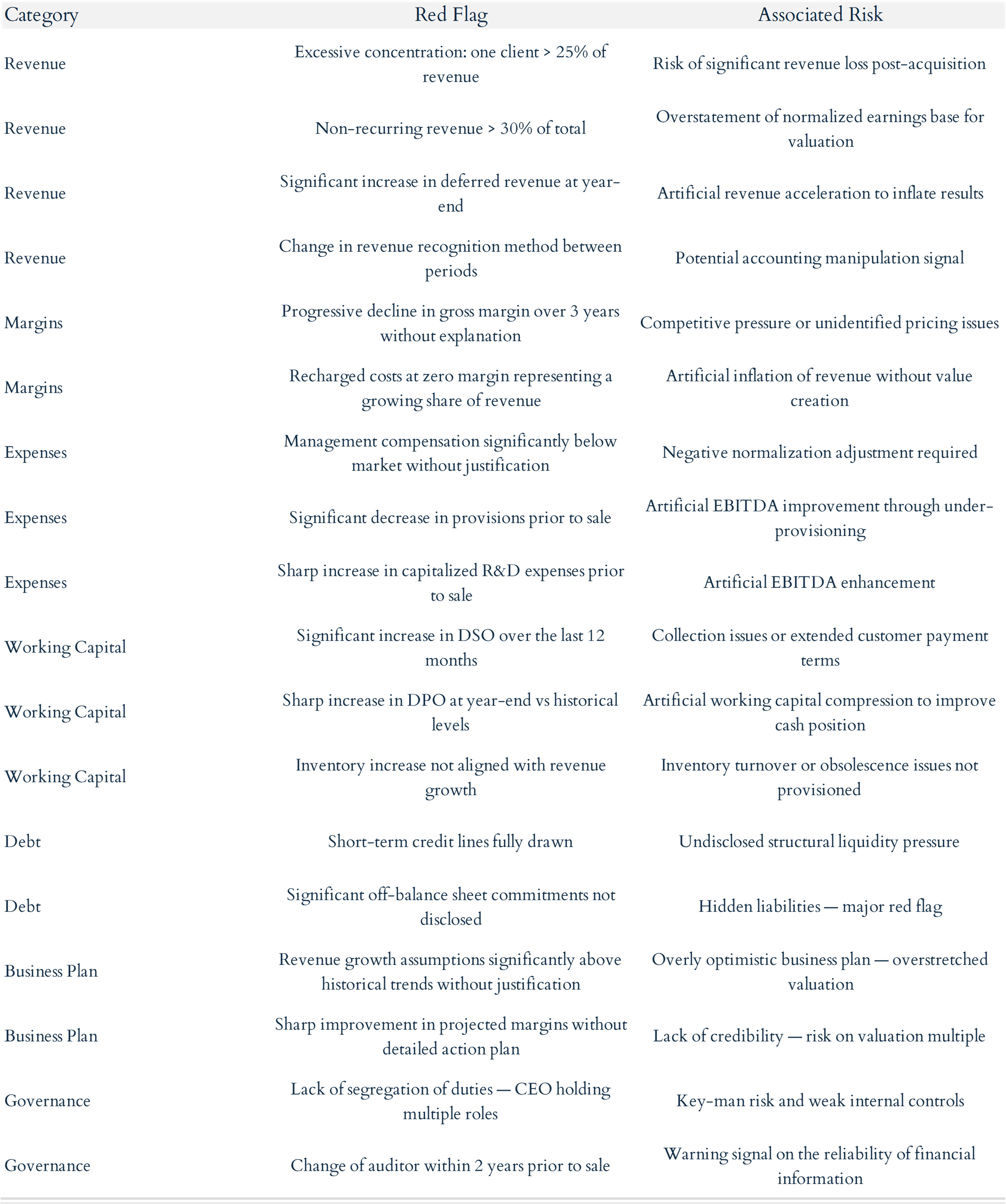

Red Flags and Warning Signals

Financial due diligence is above all a risk detection exercise. The following table presents the main red flags by category, as observed in the practice of Hectelion's missions.

Presentation of the Target

B2B SaaS software publisher specialising in data flow management for industrial SMEs. It reports revenue of €/CHF 5.2m in the last financial year, of which 78% in recurring subscription revenues (ARR), and an EBITDA presented by management of €/CHF 2,500k (48% margin). The company employs 42 people, including 18 in R&D. Its largest client represents 22% of revenue.

Main Restatements Identified

Main Adjustments on Net Financial Debt

Conclusions and Transaction Impact

Based on the due diligence work, Hectelion recommended to its buyer client the following. First, a revision of enterprise value from €/CHF 30m to €/CHF 24.9m (12x normalised EBITDA of €/CHF 2,071k). Second, an additional deduction of €/CHF 110k in respect of the identified debt-like items. Third, the inclusion in the GAP of a specific representation on the employment litigation and pension obligations. Fourth, an earn-out of €/CHF 1m conditional on achieving ARR of €/CHF 4.5m at 18 months post-closing, allowing the risk on growth projections to be shared. Fifth, a target WC clause fixed at €/CHF 320k (12-month average), with a euro-for-euro adjustment mechanism in the event of a gap at closing.

Advantages and Limitations of Financial Due Diligence

The Contributions of Financial Due Diligence

Financial due diligence is one of the best-value investments in an M&A transaction. It allows the buyer to secure its investment with verified, independent financial information, to significantly reduce the risk of post-acquisition surprises, and to have a solid factual basis for price negotiation and warranty structuring. In the vast majority of cases, due diligence fees represent a tiny fraction of the savings or protections they generate.

Limitations to Be Aware Of

Financial due diligence nonetheless has important limitations to be aware of. It does not certify the accounts and does not cover all business risks. It is conducted under time and information access constraints, meaning that some risks may not be detected — particularly when the seller does not communicate all relevant information. It is based on historical information, making it by nature poorly predictive of future risks. Finally, it does not substitute for other types of due diligence — legal, tax, operational — which are complementary and essential for a complete view of transactional risk.

CEO Message

Financial due diligence is not a process formality. It is a decision-making tool. In our practice at Hectelion, we have conducted due diligence missions that have led to price revisions of 15 to 30% compared to initial valuations — and others that have fully confirmed the quality of the target and reassured the buyer in its decision. In both cases, the value created for our client is obvious.

What distinguishes good due diligence from average due diligence is the ability to go beyond reading the accounts to understand the economic reality of the business — the real drivers of performance, the real risks, the real levers of value. It is this deep understanding that allows a robust transaction to be structured, with warranties adapted to actual risks and a price that reflects the true value of what is being purchased.

Aristide Ruot, PhD — Founder & Managing Director, Hectelion

Conclusion: Financial Due Diligence — An Indispensable Investment

Financial due diligence is the most powerful tool available to the buyer to secure its investment in the context of a merger or acquisition transaction. Whether it takes the form of a buy-side acquisition audit or a Vendor Due Diligence prepared by the seller, it constitutes the factual basis on which the entire transaction rests — from the acquisition price to contractual warranties, including price adjustment mechanisms.

Its value lies less in the production of a report than in the quality of the analysis it generates — an analysis that must go beyond reading the accounts to reveal the economic reality of the business, identify hidden risks, and provide the elements necessary for an informed acquisition decision. In an increasingly competitive M&A environment, where processes accelerate and information becomes more complex, financial due diligence is not a luxury — it is a necessity.

Looking to build expertise in Mergers & Acquisitions?

Hectelion offers M&A training programs combining theoretical foundations, practical methodologies, and real-life transaction case studies.

👉 Learn more about the program

Author

Aristide Ruot, Ph.D

Founder | Managing Director

.jpg)